Pralana Online User Manual** **Last updated: 3/1/2026

Introduction

Pralana is a sophisticated, high-fidelity financial planning platform designed to model your financial future in as much—or as little—detail as you choose. Pralana provides insight into a range of possible outcomes, enabling more informed financial decisions.

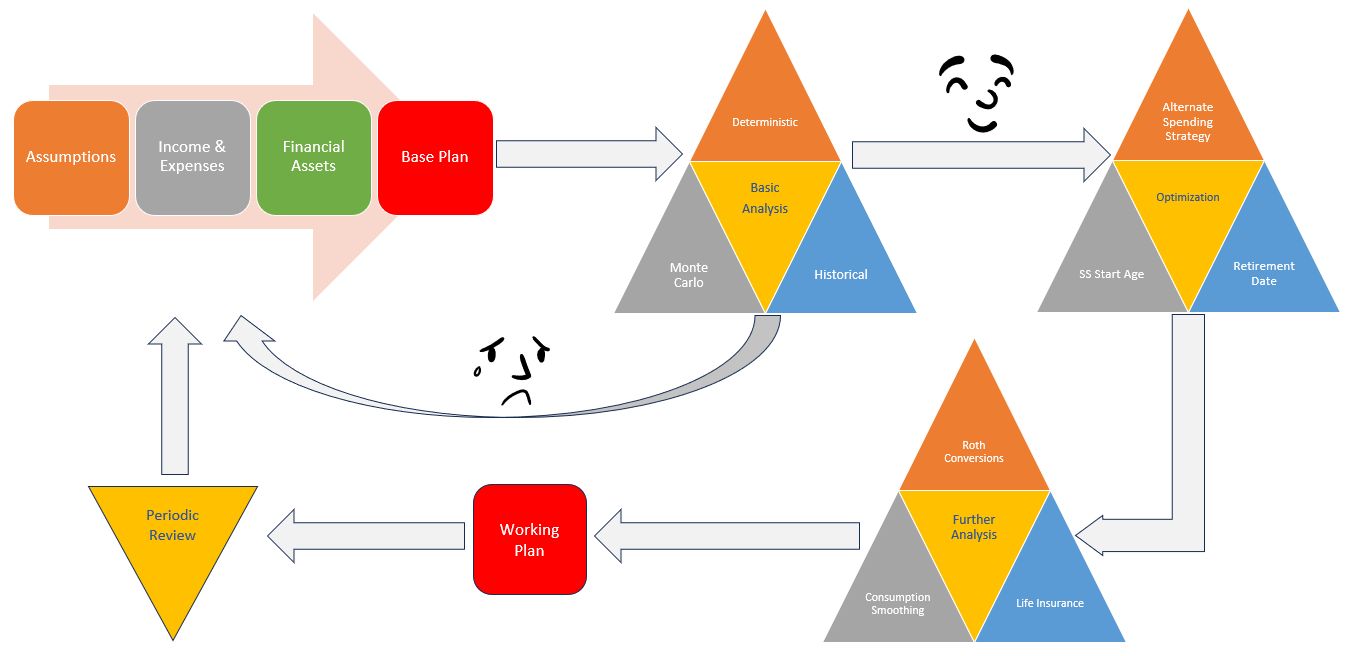

This user manual will help you understand how Pralana is organized and how to get the most value from its extensive capabilities. Most users begin by creating a base plan, then iteratively refine it—examining alternatives, exploring “what-if” scenarios, and optimizing decisions—until they arrive at a working plan. From there, your plan can be easily revisited, reviewed, and refined over time as circumstances, assumptions, or goals change.

The planning process within Pralana follows these steps:

Build – Enter personal and family information, define key assumptions, and provide details about assets, income, and expenses to establish a base plan.

Review & Analyze – Run initial analyses to assess plan viability, including the probability of not outliving your assets.

Refine & Optimize – Adjust inputs, explore alternatives, and apply optimization tools to arrive at your working plan.

Revisit – Periodically return to your plan to update assumptions, reflect new information, and re-analyze outcomes.

Subscription Levels

Pralana offers three subscription types for different needs. Each subscription supports one or more plans. Plans may include up to three scenarios test alternative income, expense, account growth and other assumptions.

Platinum: supports a single plan

Platinum Family: allows you to create up to 5 separate plans for yourself and others.

Platinum Pro: adds plan-management features for financial advisors and is offered in tiers supporting 25, 50, and 100 simultaneously active clients.

Key Features

Pralana’s depth of features and calculation transparency distinguish it from many other financial planning tools.

Sources of Income:

Employment, pensions, Social Security, annuities, windfalls, and miscellaneous income.

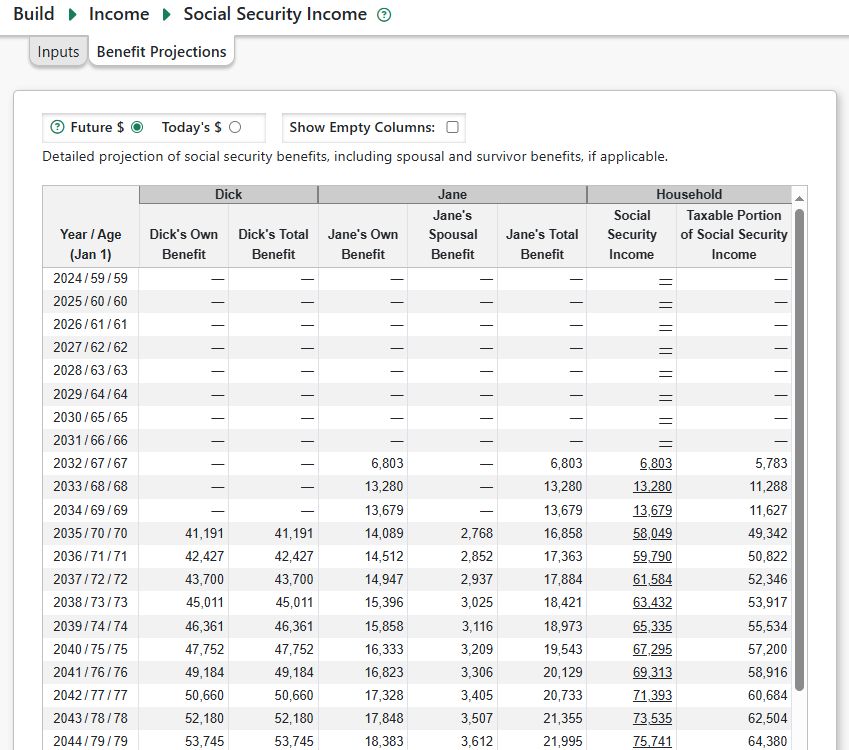

Social Security benefits, including spousal and survivor benefits, are calculated based on your start ages and your benefit at your full retirement age.

Expenses:

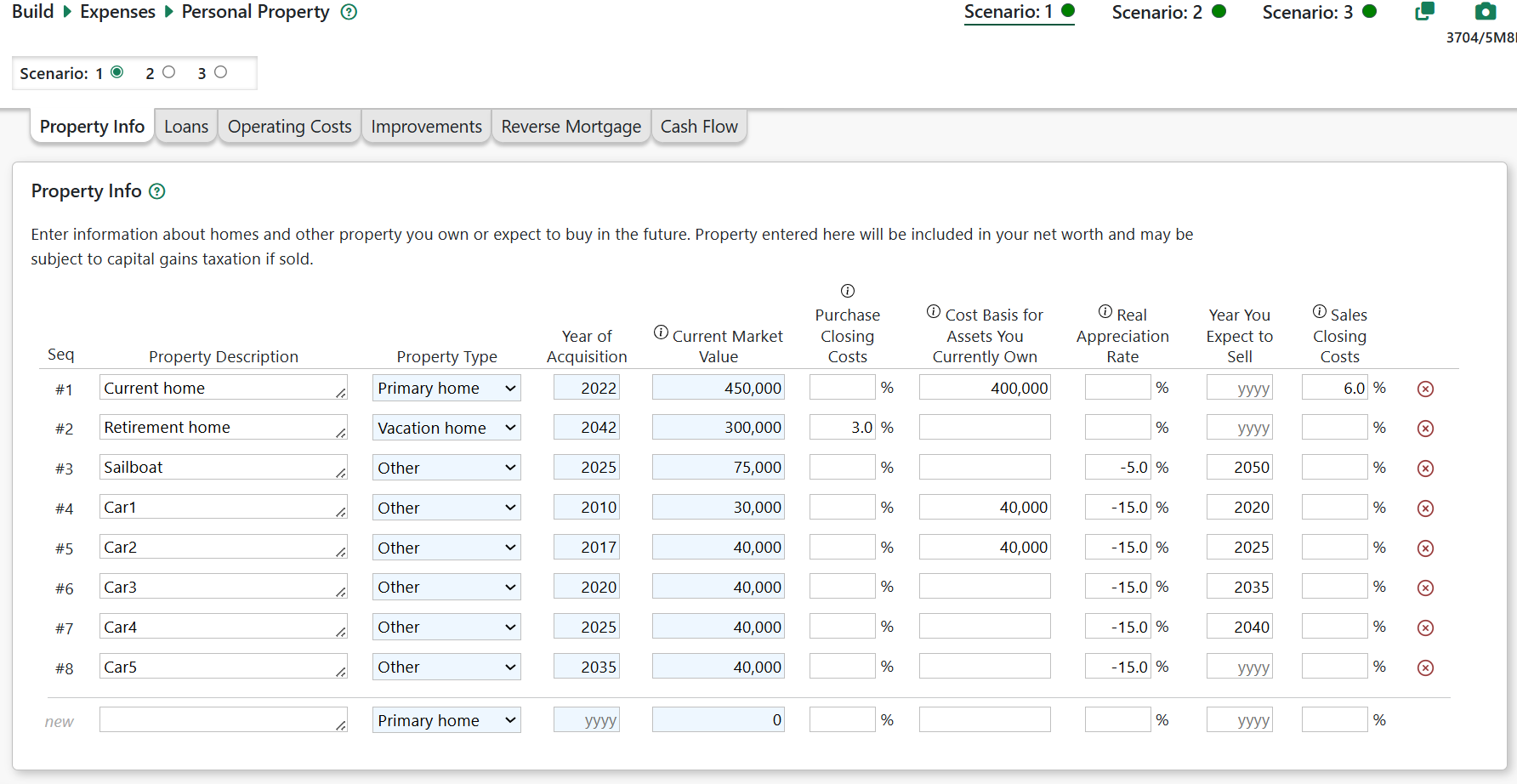

Personal property and rental property, including user-defined operating costs and capital improvements.

Children’s expenses, including college tuition, loans and 529 college savings plans.

Healthcare expenses, including auto-calculation of Medicare premiums and IRMAA, ACA subsidies and support for Health Savings accounts.

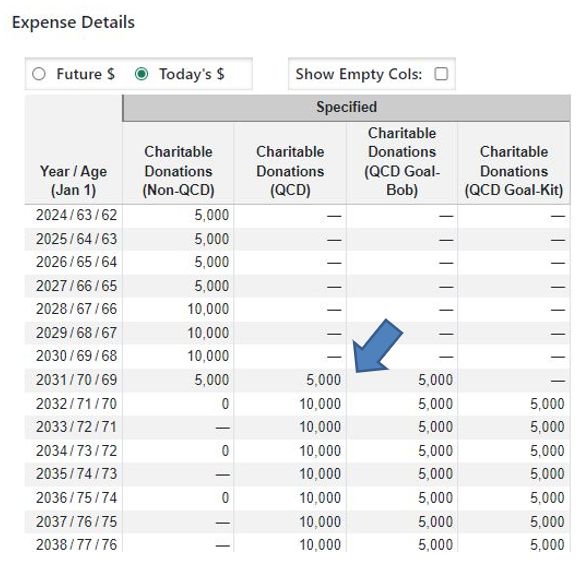

Charitable giving, including QCDs from your IRAs and inherited IRAs.

User-defined expenses. Each may be categorized as essential or non-essential and you may specify different inflation assumptions and other parameters.

Loans: Purchase, refinance, home equity loans and HELOCs on personal and rental property.

Investment loans as well as personal loans made by you to others.

All loans support interest-only periods, additional principal payments, early payoff, and user-defined tax deductibility of interest.

Insurance:

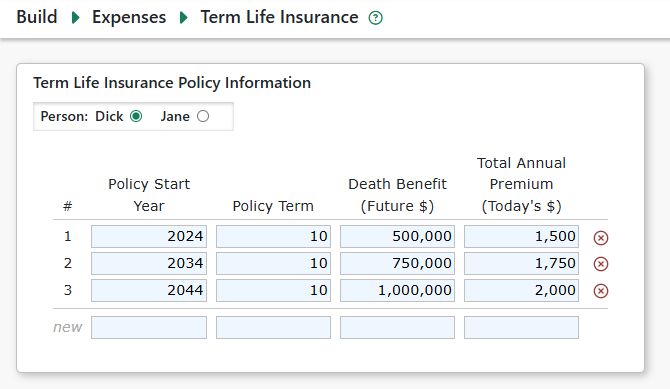

Term and cash-value life insurance modeling.

Accounts:

Eleven types of accounts including cash, taxable, tax-deferred (401k, IRA, etc.), Roth IRAs and inherited traditional and Roth IRAs.

Calculation of RMDs for tax-deferred and inherited traditional IRAs.

Scheduled account transfers of funds between accounts as well as transfers of appreciated assets to external organizations.

User-defined account withdrawal order to cover cash shortages.

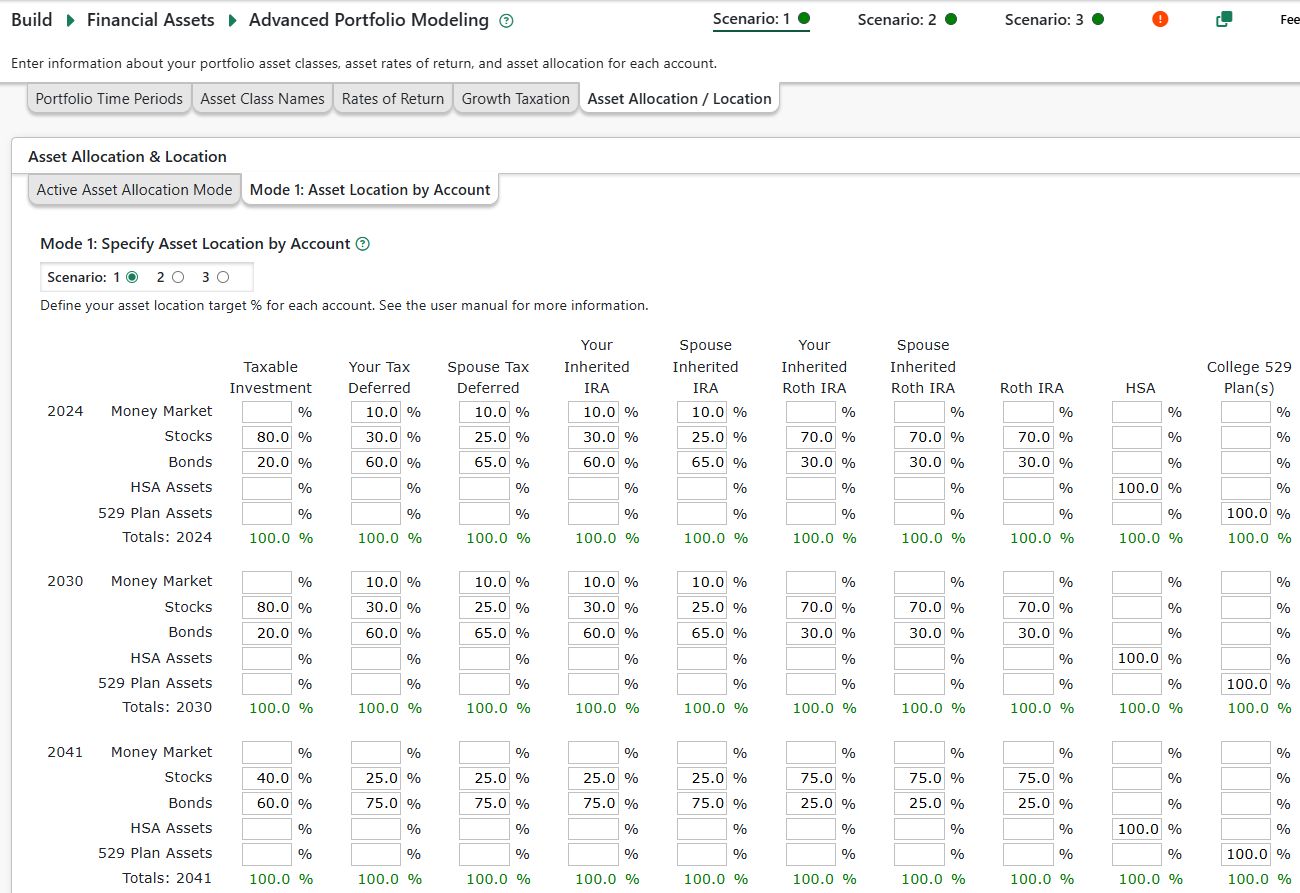

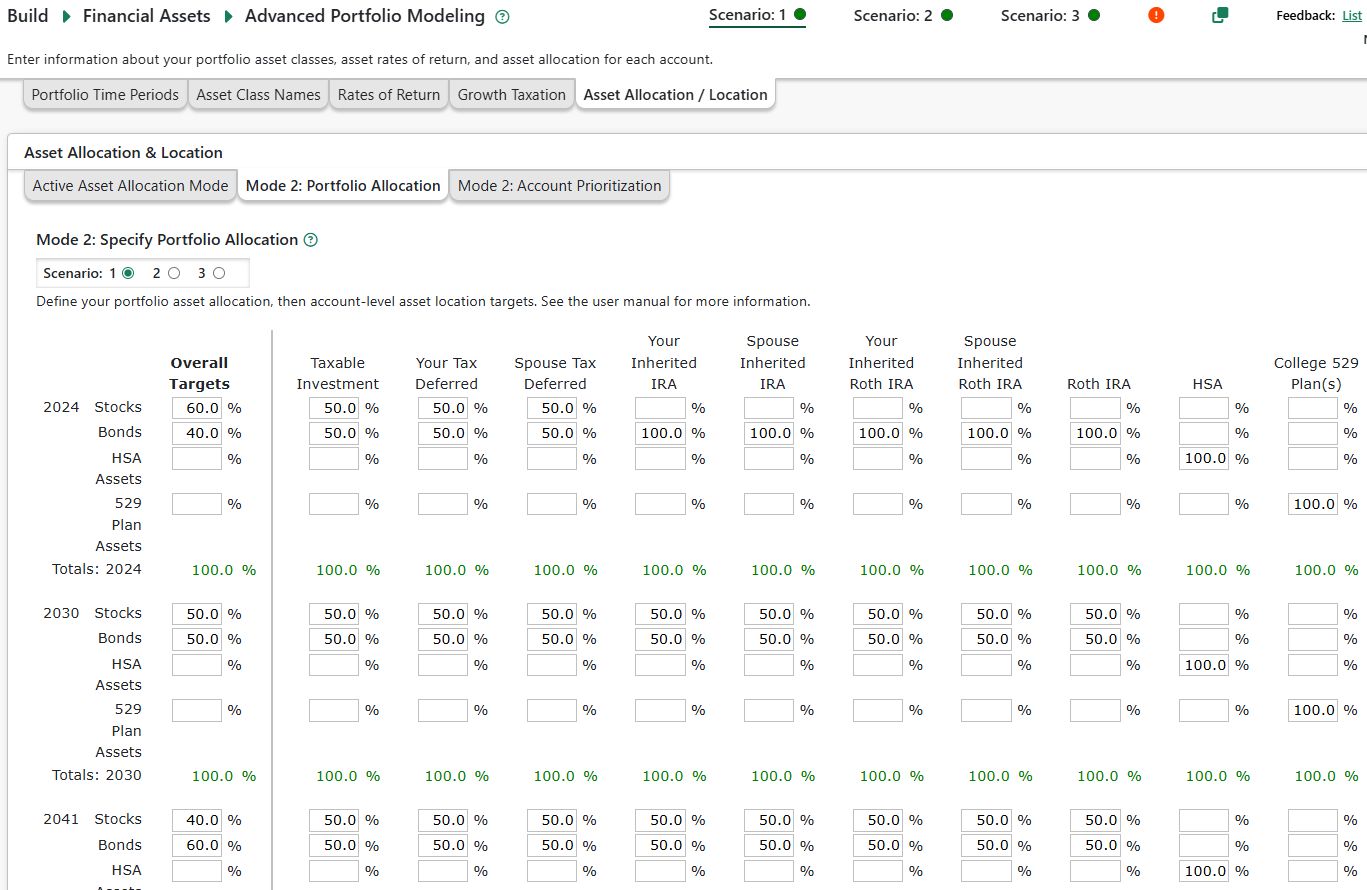

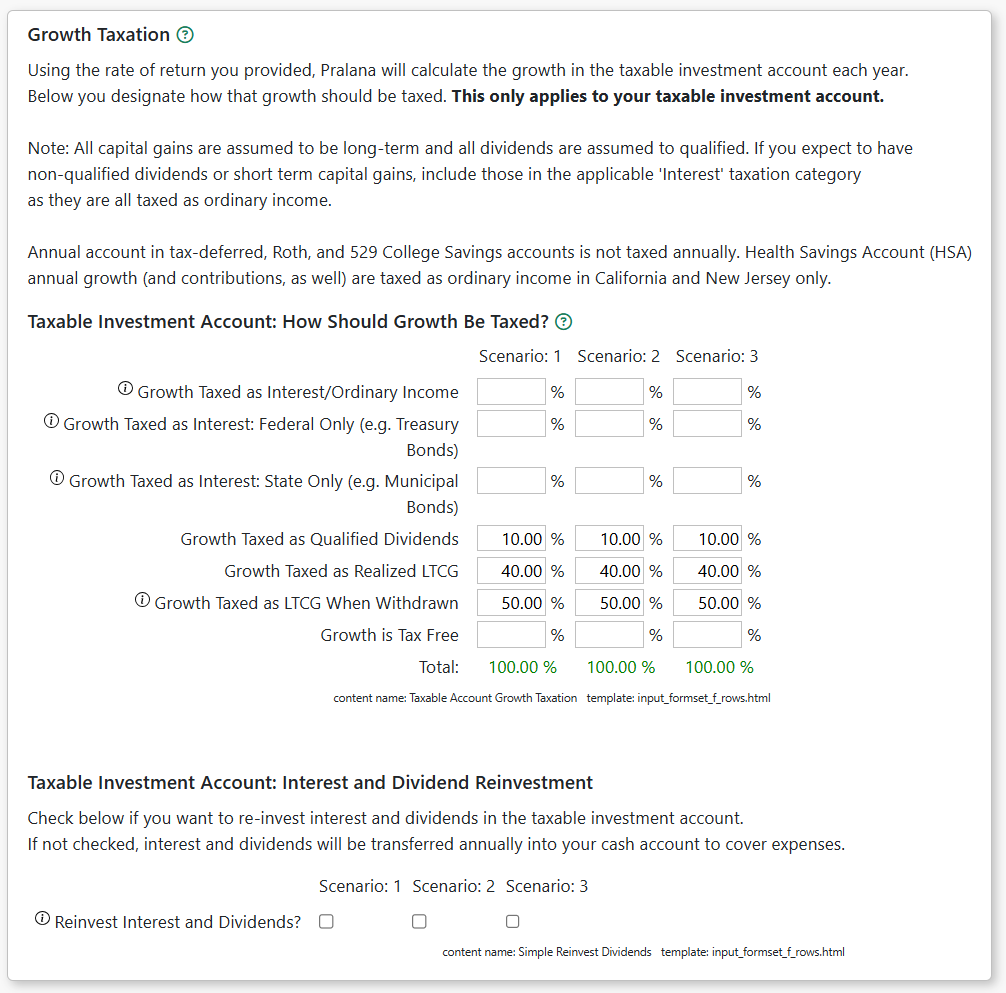

Simple and advanced portfolio growth modeling using rates of return by account or user-defined asset classes. Seven options to categorize how growth in taxable accounts is taxed.

Analysis and Optimization Tools:

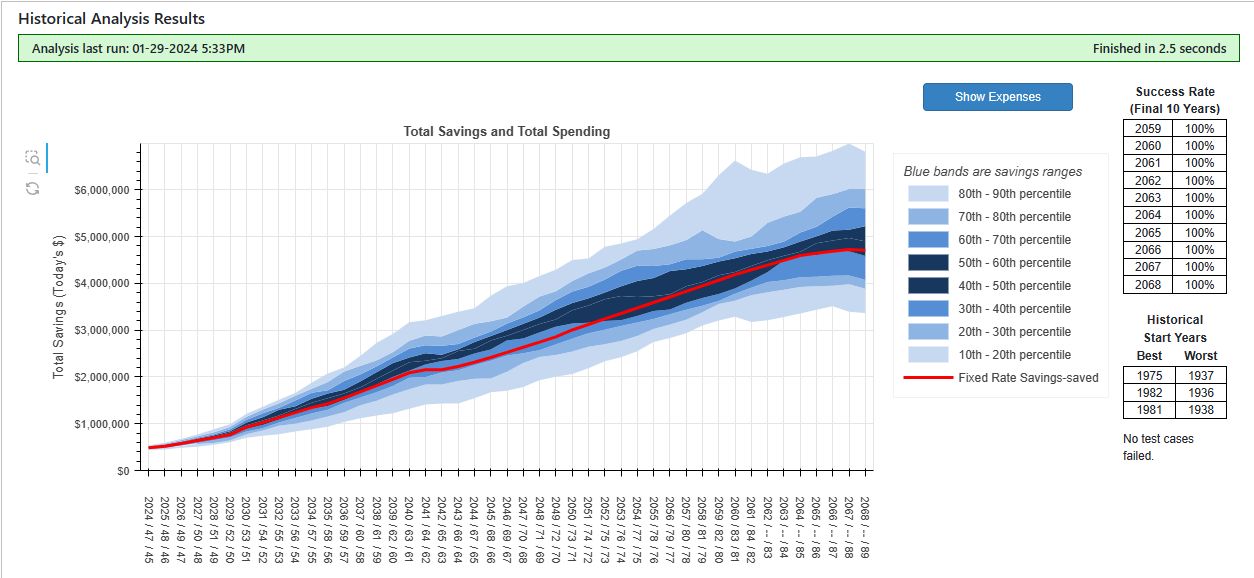

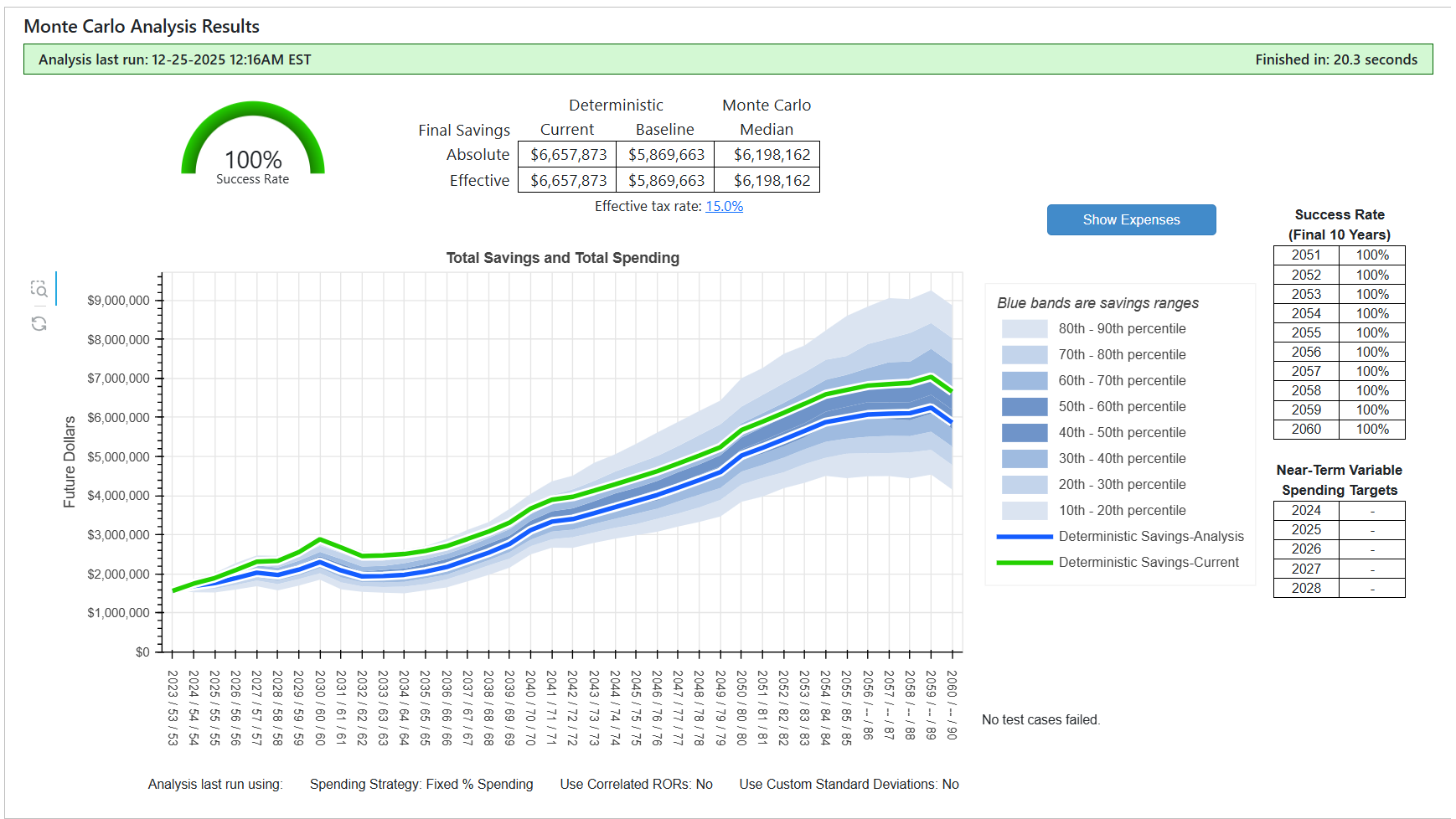

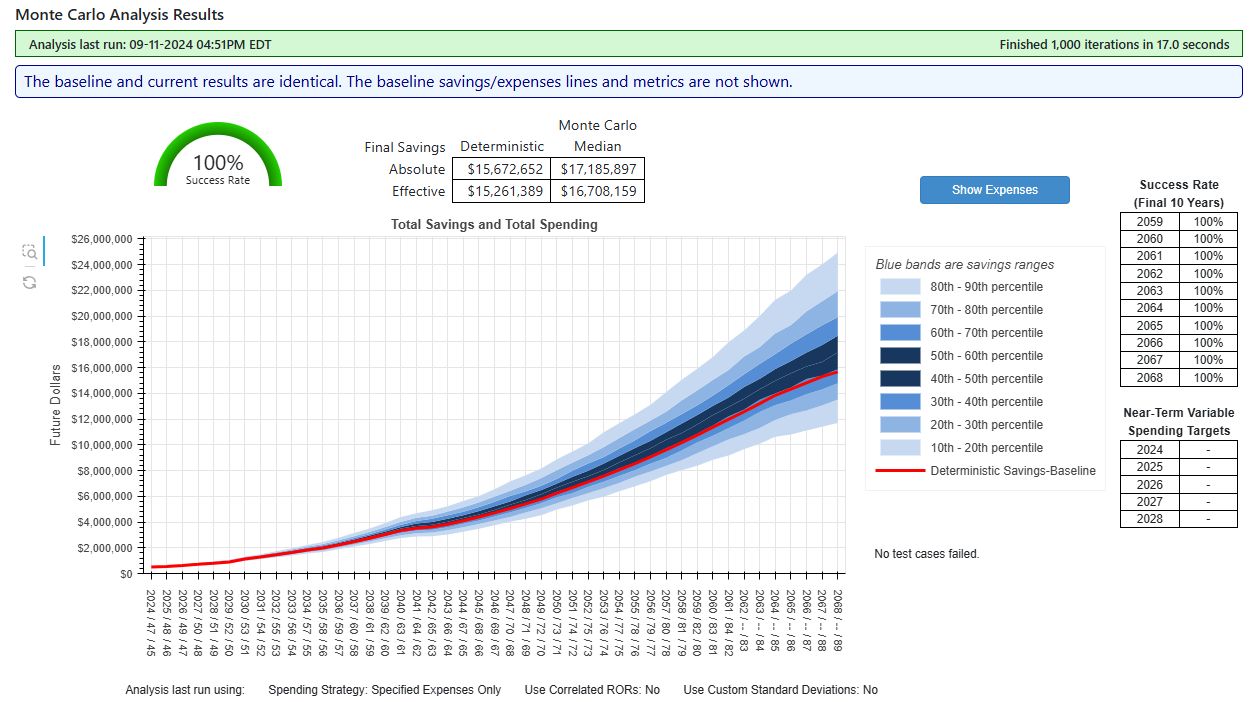

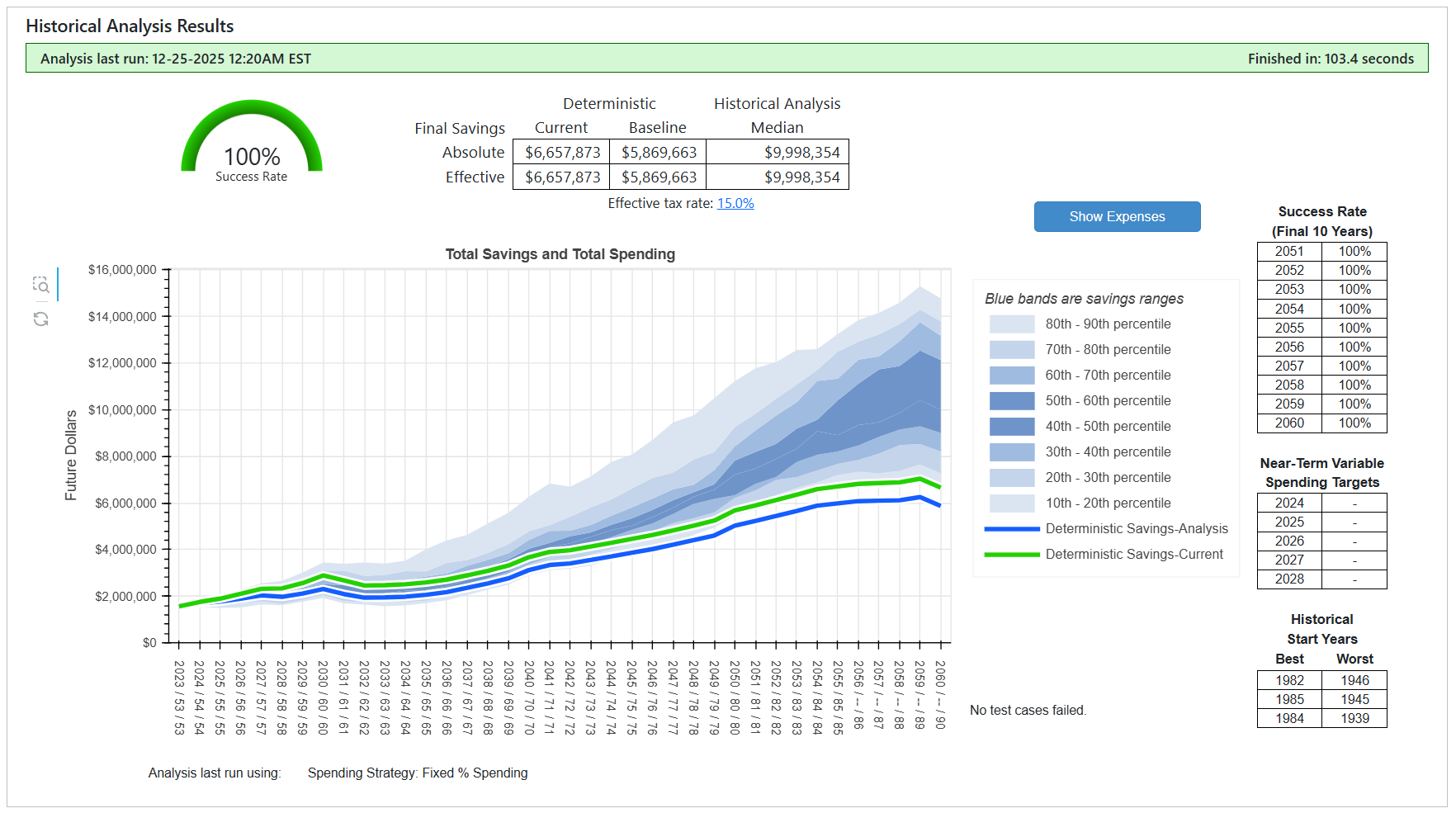

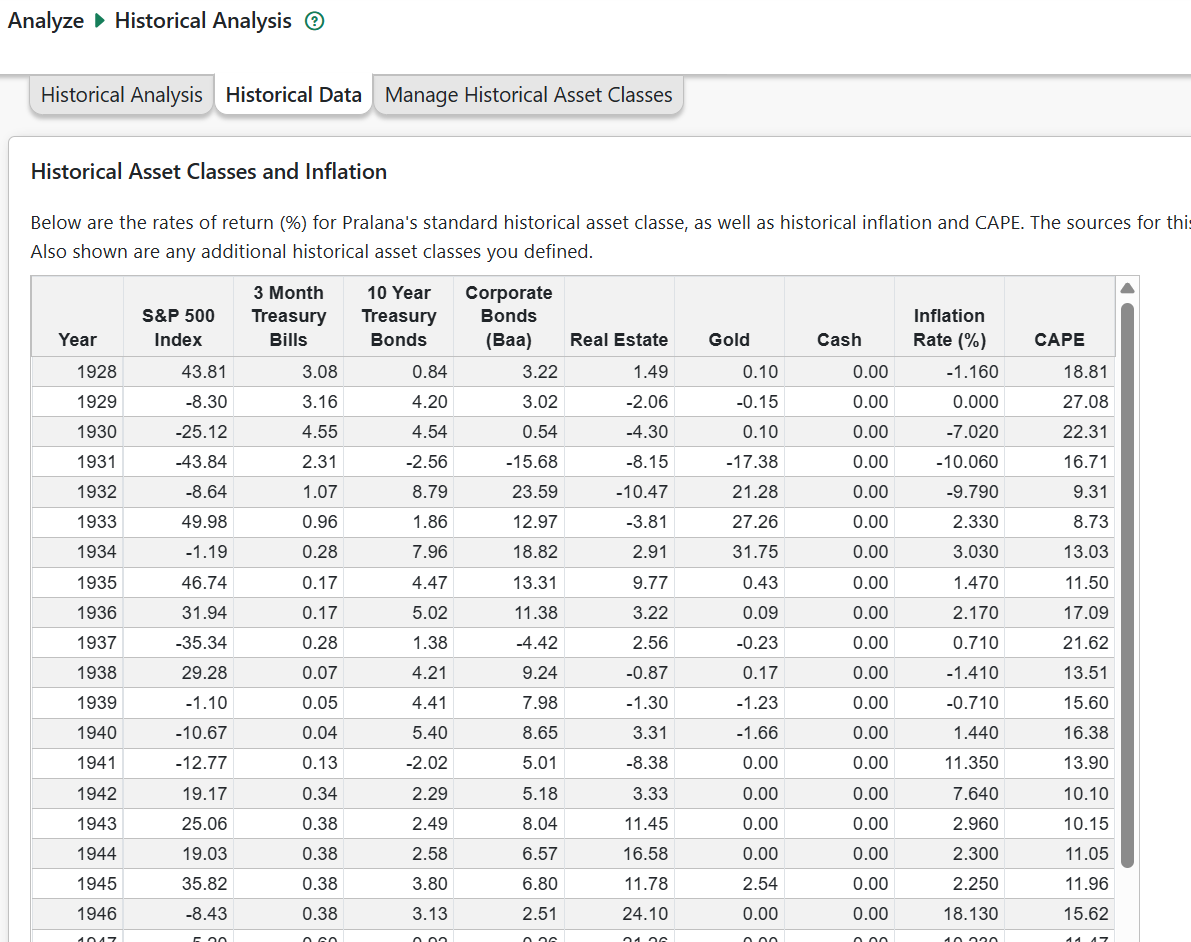

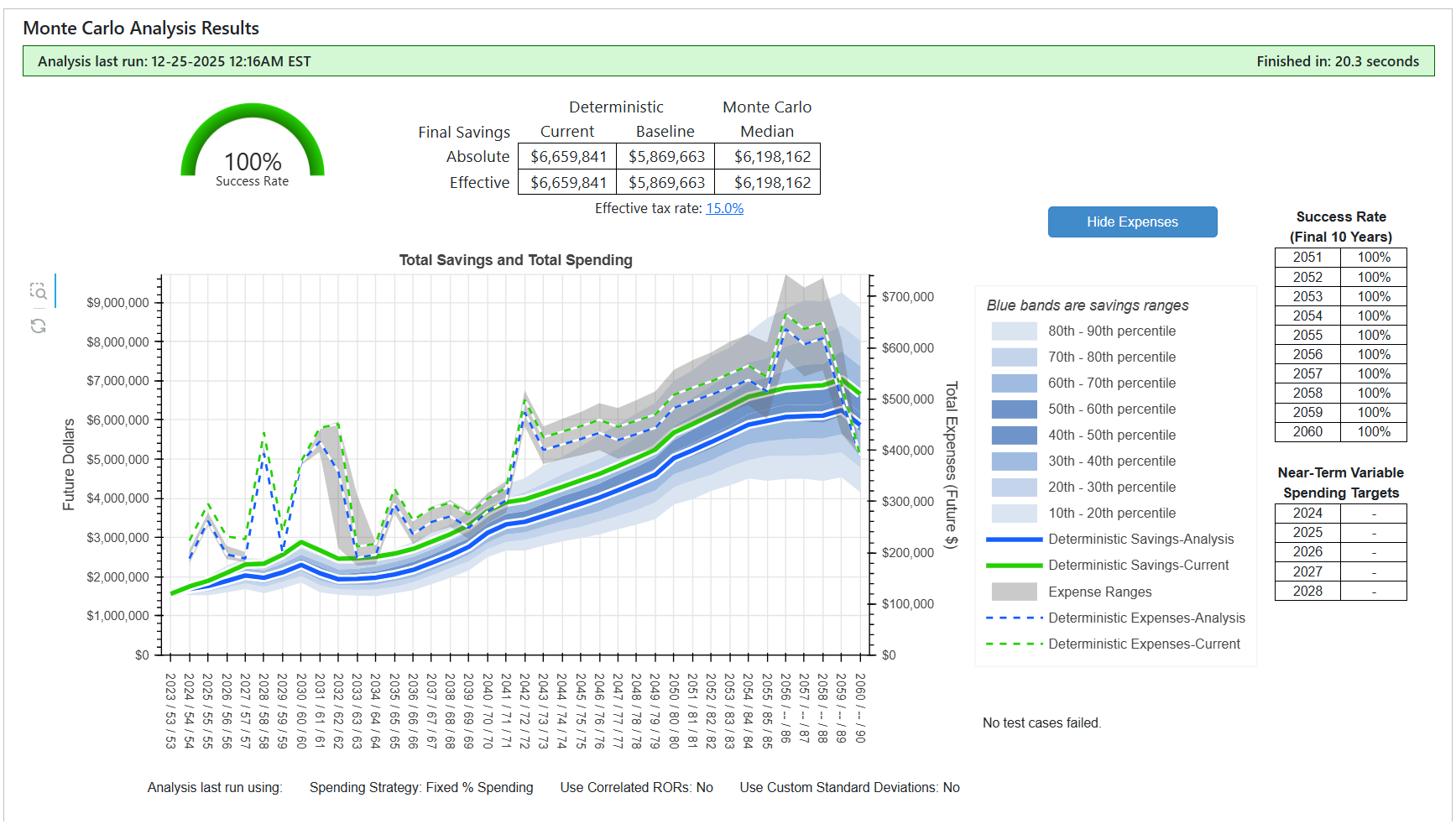

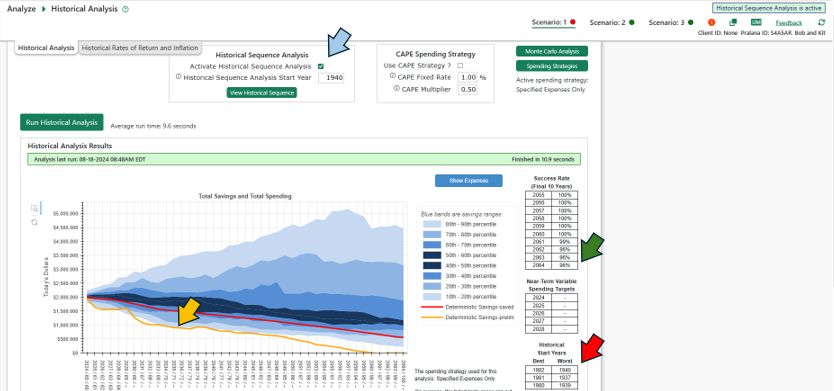

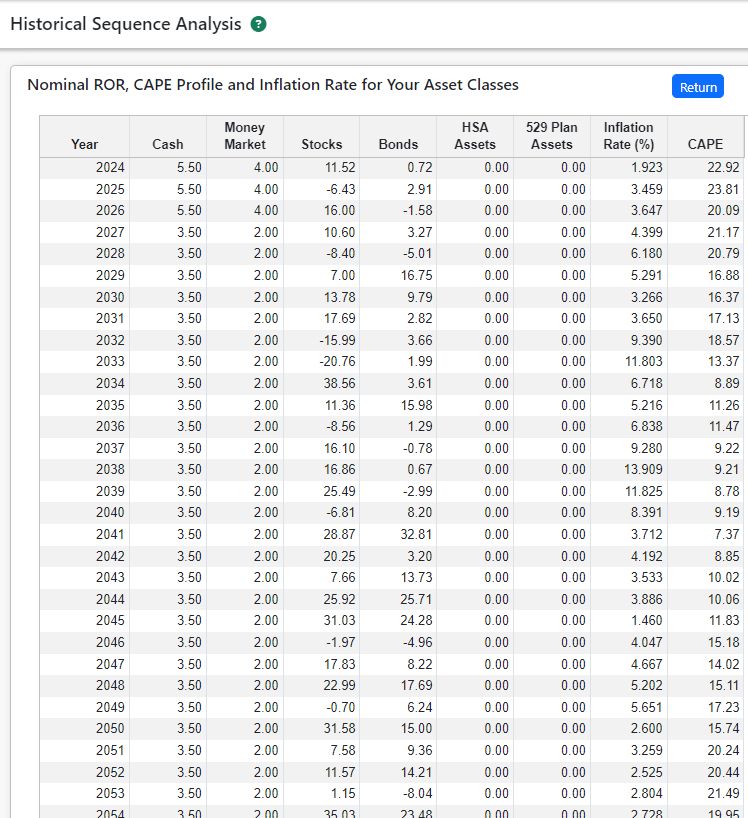

Monte Carlo and historical analyses provide a way to test scenarios using randomized or historical rates of return.

Historical sequence testing, allowing you to evaluate your plan against some of the worst market periods on record.

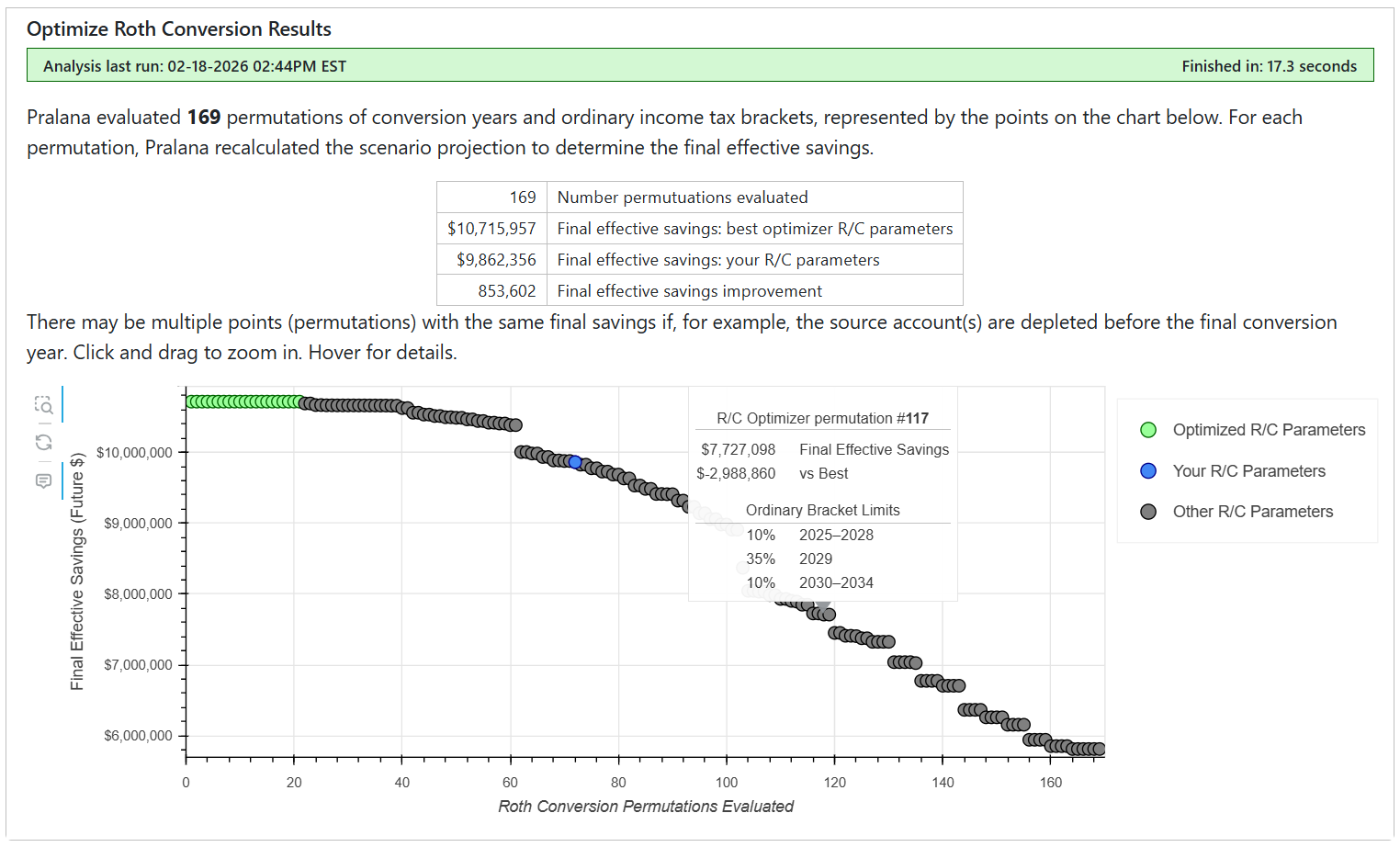

Roth conversion planning and optimization, including constraints by user-specified tax brackets, capital gains brackets, IRMAA thresholds, and ACA Federal Poverty Level multiples.

Social Security start age optimization.

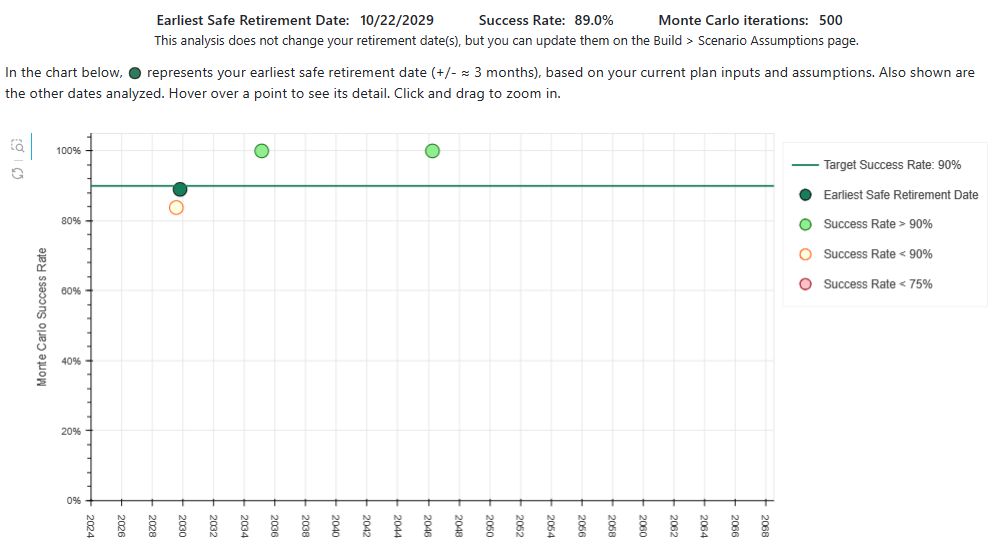

Earliest safe retirement date analysis.

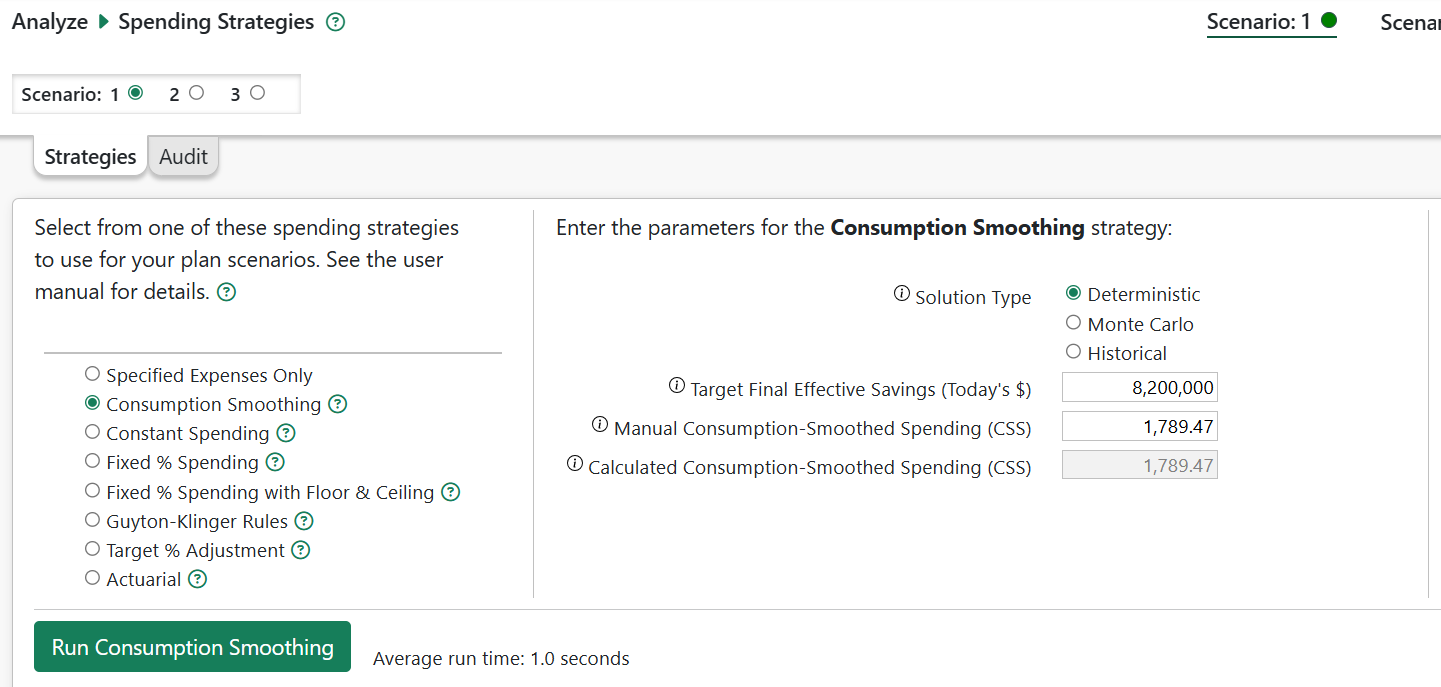

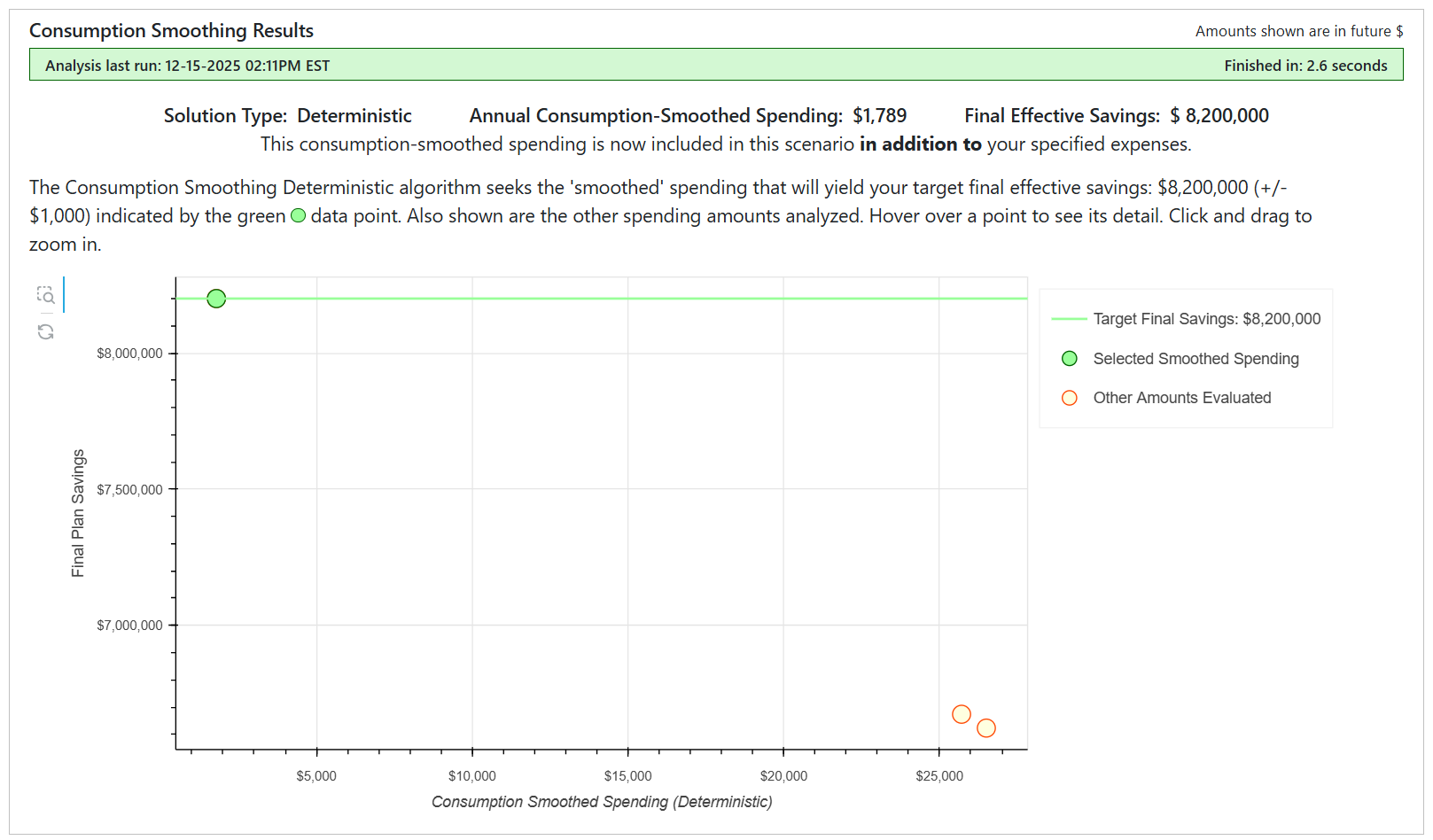

Seven variable spending strategies: consumption smoothing, constant spending, fixed % spending, fixed % spending with floor & ceiling, Guyton-Klinger, target % adjustment and actuarial. These strategies dynamically adjust spending during retirement based on portfolio performance.

Results Views:

Interactive charts illustrate projected income, expenses, savings, net worth, taxes and more.

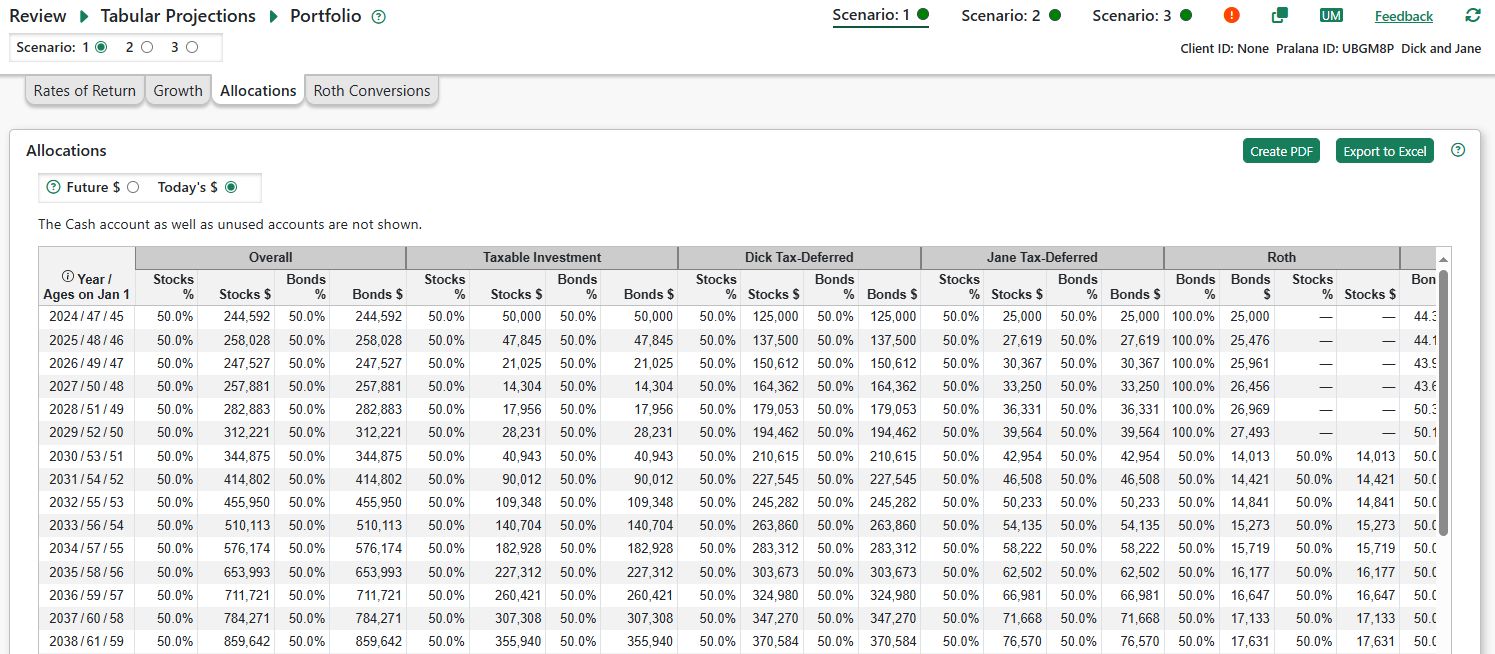

Rich tabular projections, including detailed year-by-year income, expense, cash flow, balance sheet, and asset allocation views.

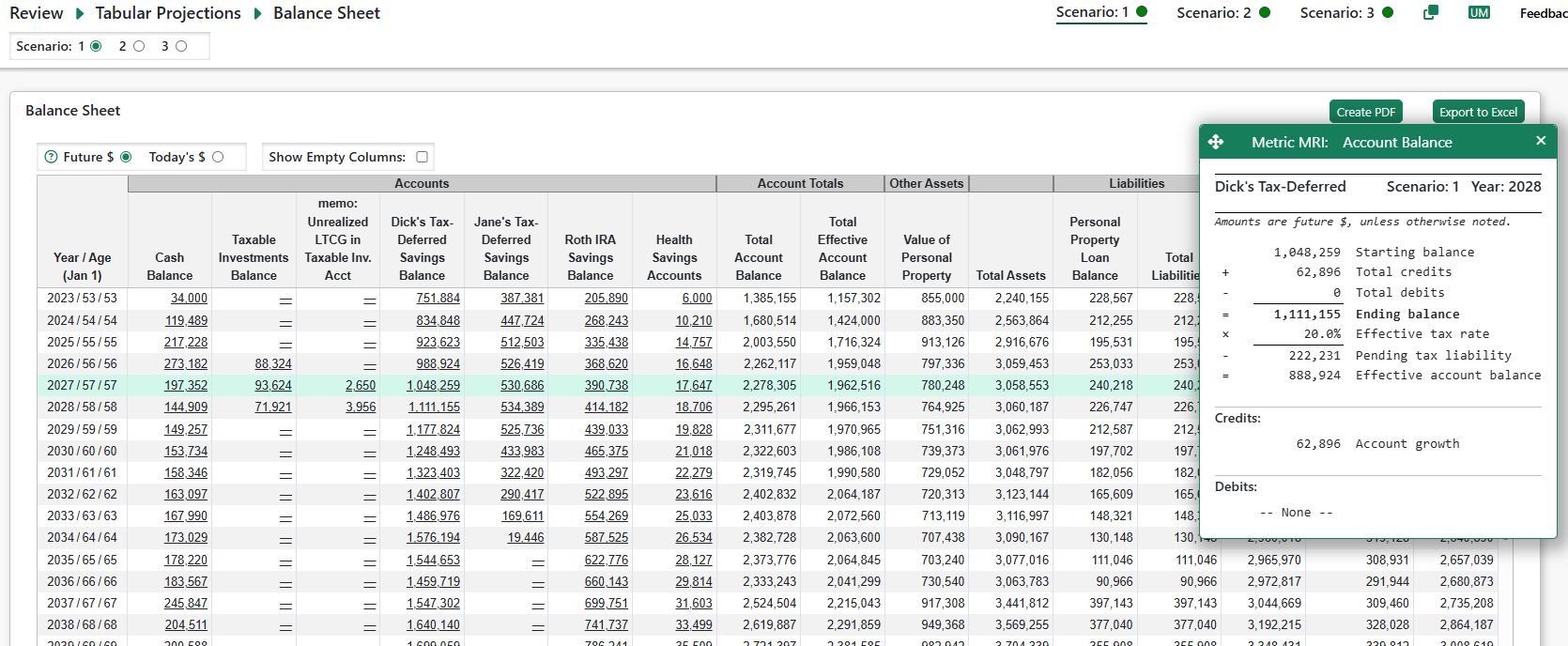

Pralana’s “Metric MRIs,” available for tabular projections and tax forms, provide transparency by showing how key values—such as Social Security income, account balances, healthcare costs, and Roth conversions—are calculated.

Report generation and export to Excel and PDF, enabling printing and sharing of your plan.

Tax Forms Supported by Pralana:

Pralana estimates your Federal, state and local tax liability each year and shows you a representation of the forms listed below. More forms may be added over time.

1040 U.S. Individual Income Tax Return Federal forms and schedules: 1040 Personal Exemption Worksheet 1040 Schedule 1 Additional Income and Adjustments to Income 1040 Schedule 2 Additional Taxes Schedule A Itemized Deductions Schedule D Capital Gains and Losses Schedule E Supplemental Income and Loss 4797 Sales of Business Property 6251 Alternate Minimum Tax 8582 Passive Activity Loss Limitations 8606 Nondeductible IRAs 8812 Credits for Qualifying Children 8960 NIIT 8962 ACA Premium Tax Credit 8995 QBI Deduction |

Unrecaptured Section 1250 Gain Worksheet Federal worksheets: Schedule A Home Mortgage Interest Worksheet Schedule A Itemized Deductions Worksheet Schedule D Capital Loss Carryover Worksheet Schedule D Tax Worksheet 1040 Qualified Dividends and Capital Gains Worksheet Pub 915 Figuring Your Taxable SSI Benefits 6251 AMT Exemption Worksheet 8812 Credit Limit Worksheet A State and local forms: State Generic Tax Return Local Generic Tax Return GA Form 500 Schedule 1 Page 2 Retirement Income Exclusion GA Form 500 Schedule 1 Page 3 Military Retirement Income Exclusion |

|---|---|

Scenarios in Pralana

Pralana is a powerful decision-making tool that lets you model different assumptions and evaluate their long-term impact. In Pralana, a ‘scenario’ is a complete set of assumptions, income sources, and expenses. Pralana allows you to define up to three scenarios and compare their results.

On most pages, only inputs or projections for one scenario is visible at a time. You select the active scenario using the radio buttons near the top of the page. This lets you enter different values for the same fields across scenarios—such as life expectancy, inflation, asset allocations, income streams, and expenses.

All scenarios share a common set of key plan-level input such as demographic information (your name, date of birth) and initial account balances.

Income and expenses as well as asset allocations and rates of return may be defined differently for each scenario.

Results are shown graphically and in detailed tables to help you compare possible outcomes. Most tabular projections provide the option to compare metrics from two or more scenarios.

Create an additional scenario: go to Build > Scenario Assumptions > Add/Delete Scenarios and enter a name and description.

The new scenario will be created with a few values copied from Scenario 1. The scenario radio buttons will then appear on all input pages, allowing you to select which scenario to modify, view and run analyses.

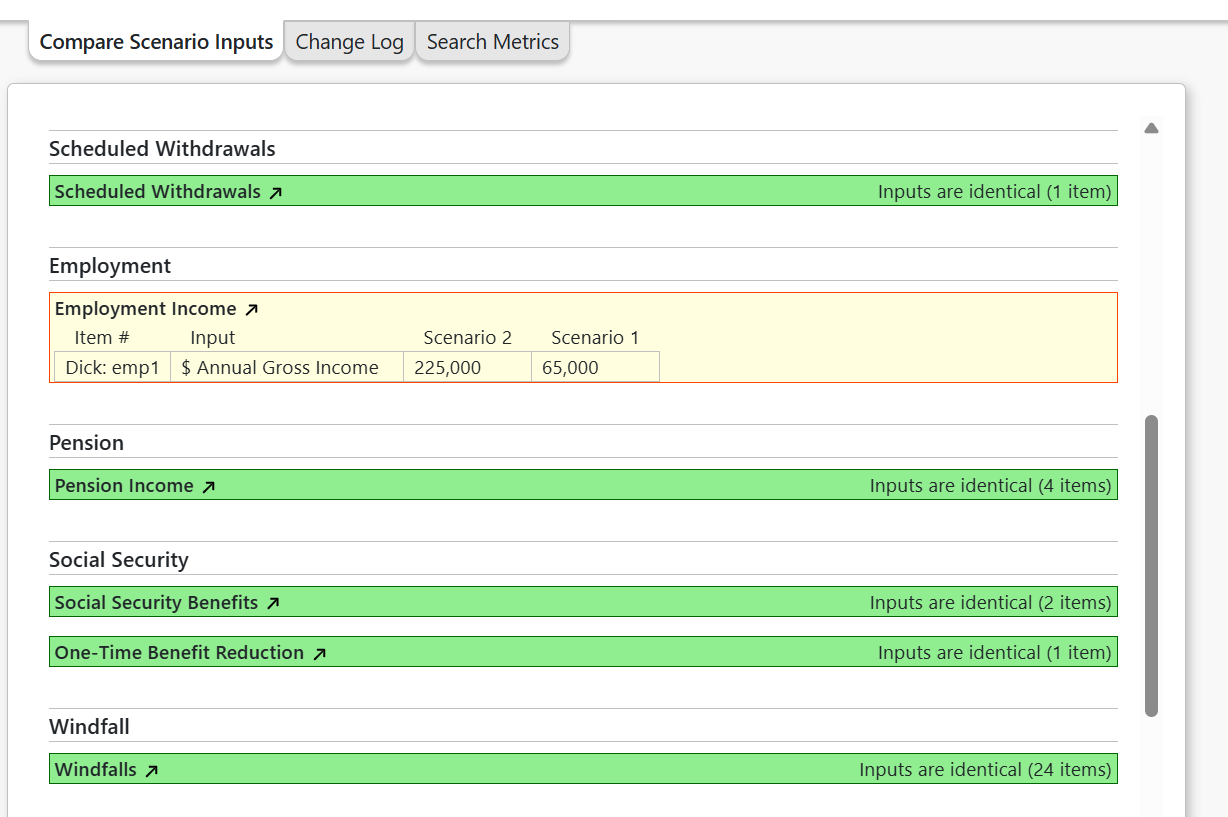

Pralana provides tools to help you compare your scenario inputs and projections as well as copy inputs between scenarios.

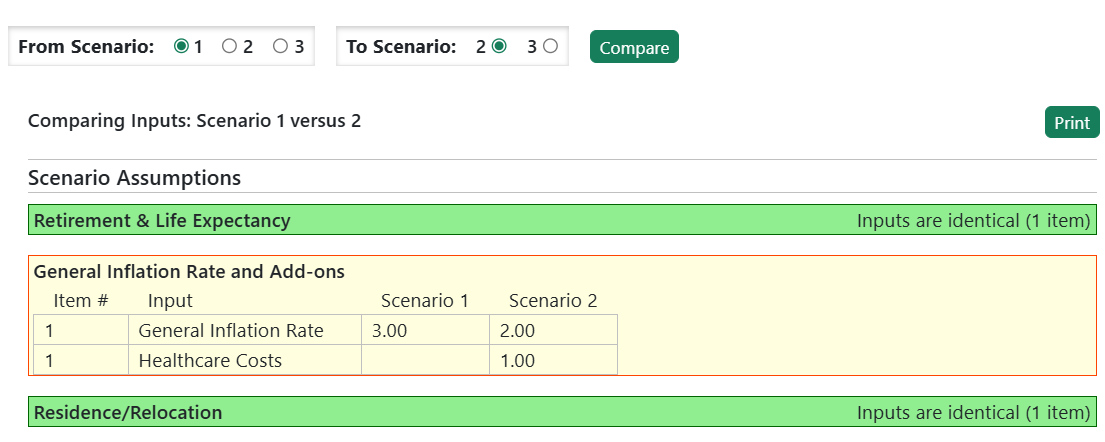

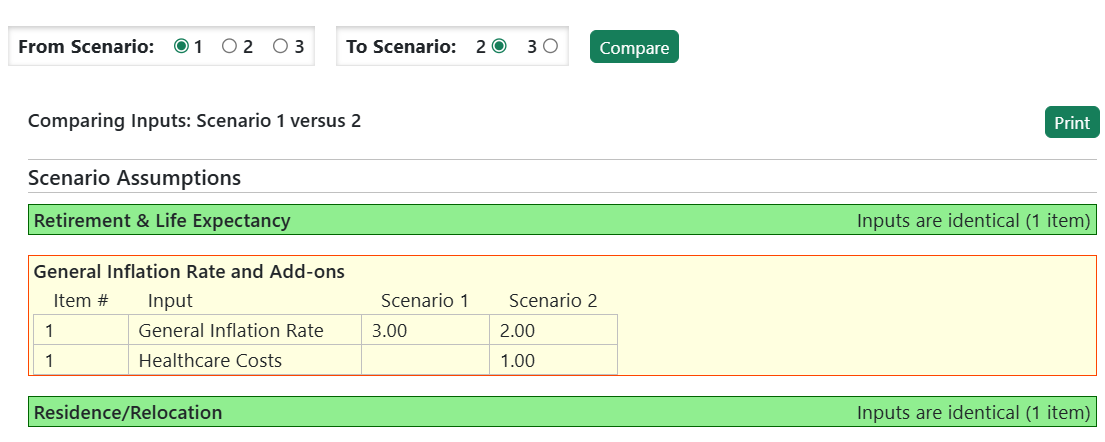

Compare Scenario Inputs

This page shows a comparison of the inputs for two selected scenarios, highlighting differences. It is organized by input page, with links to those pages.

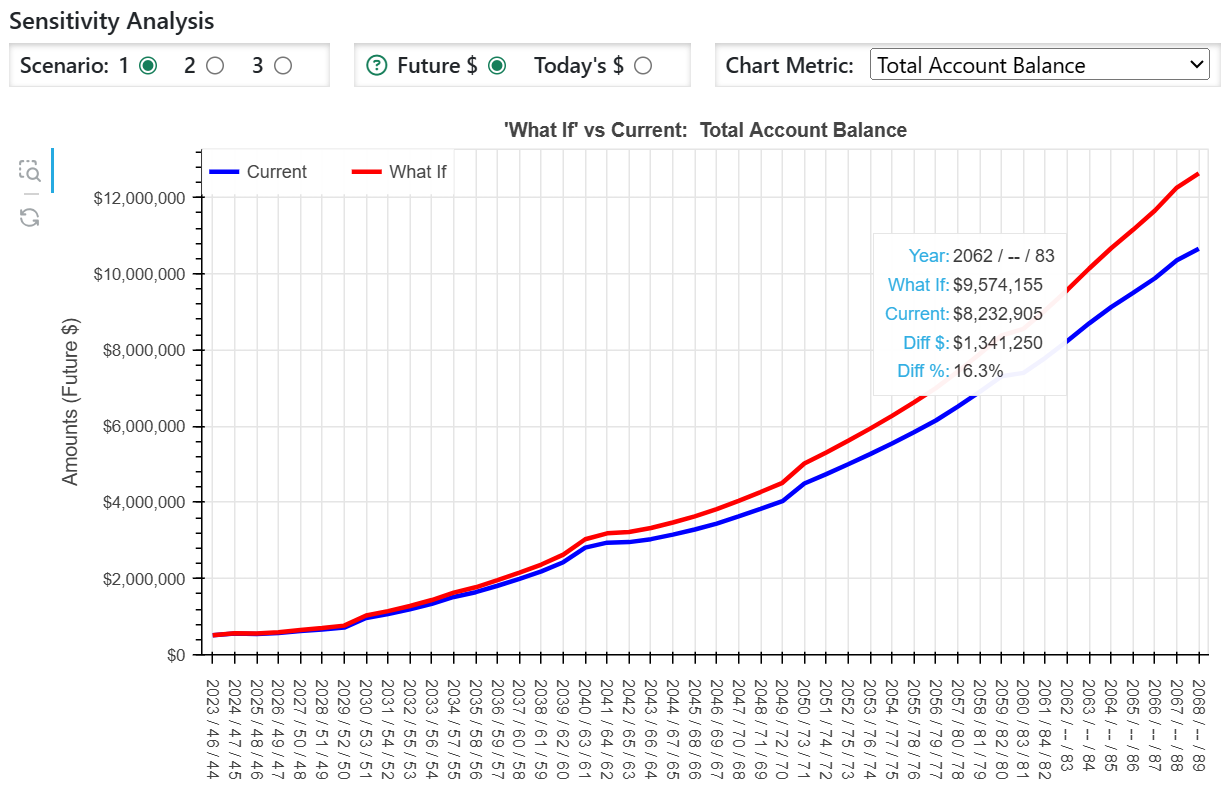

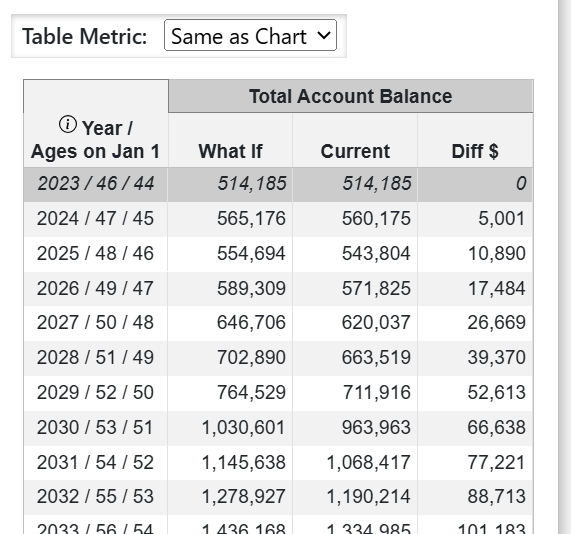

Compare Scenario Results

This page, available at Review > Graphical Projections, includes a chart and table that shows projection of key metrics for the selected scenarios. Controls on this page:

Compare to Scenario: If your plan has more than one scenario, select the scenario(s) you want to compare to the currently active scenario.

Chart Metric: Select from one of several metrics to display on the chart.

Table Metric: Select ‘Same as Chart’ to have the table show the chart data, highlighting differences in the metric values by year. Select ‘All’ to have the table show all available key metrics.

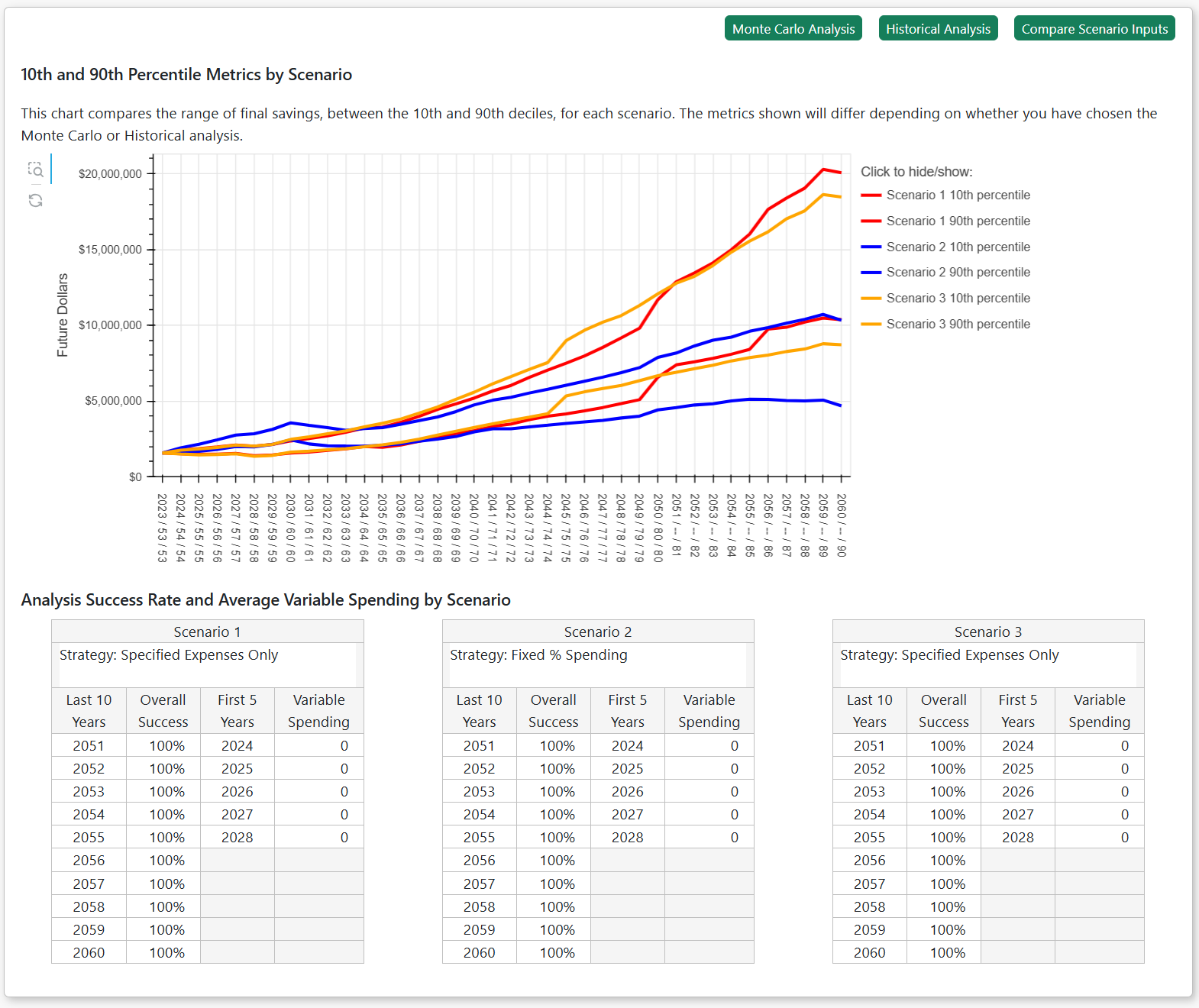

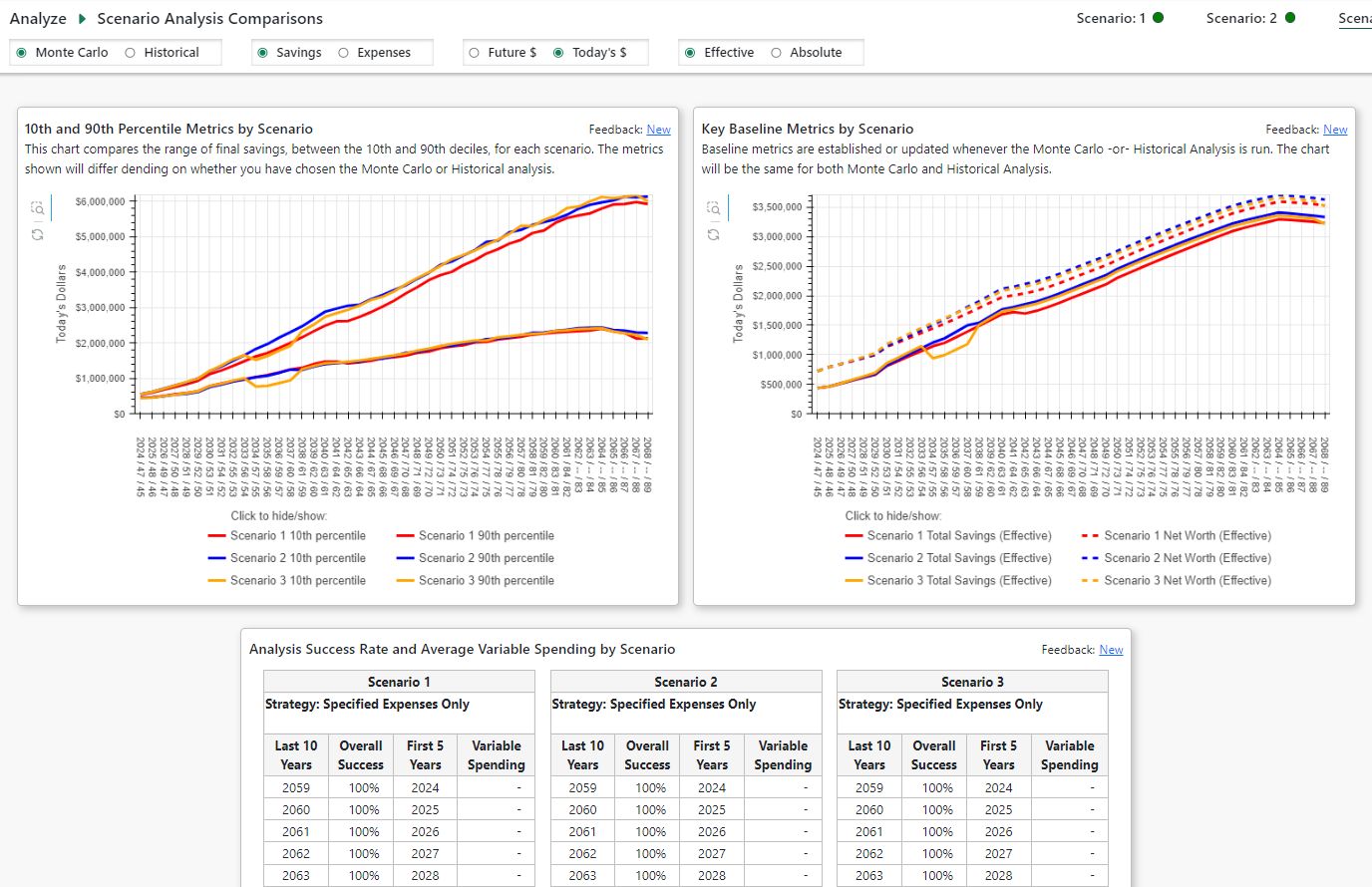

Scenario Analysis Comparisons

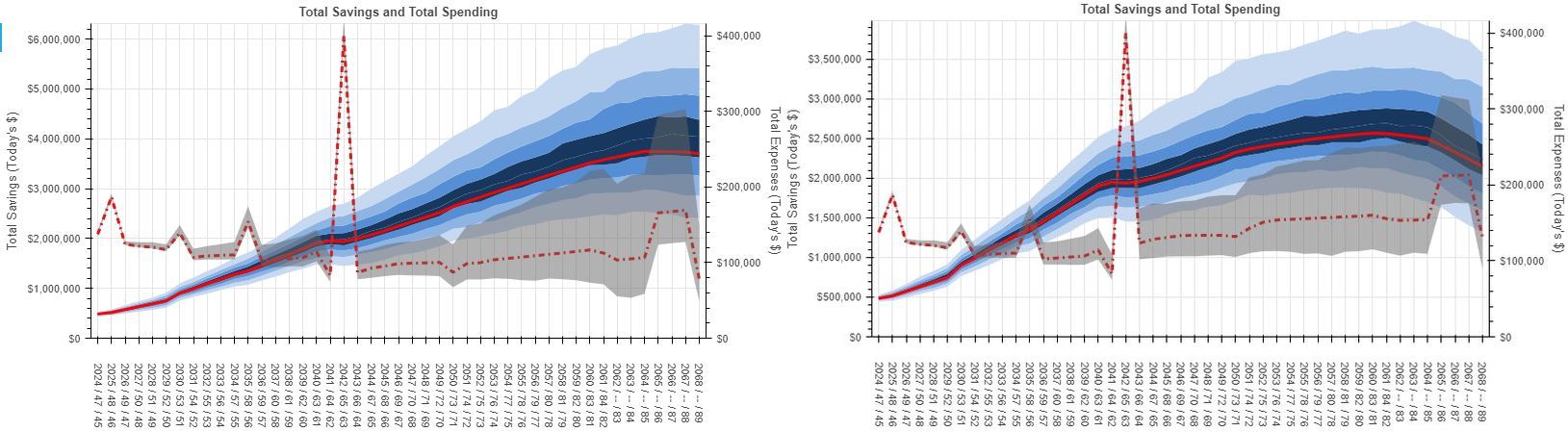

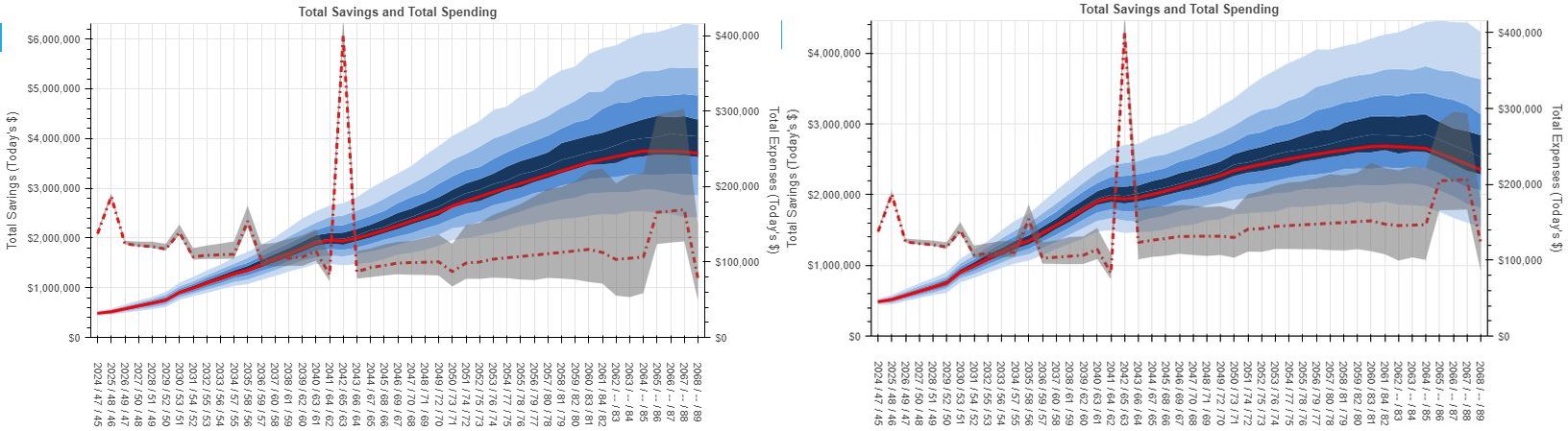

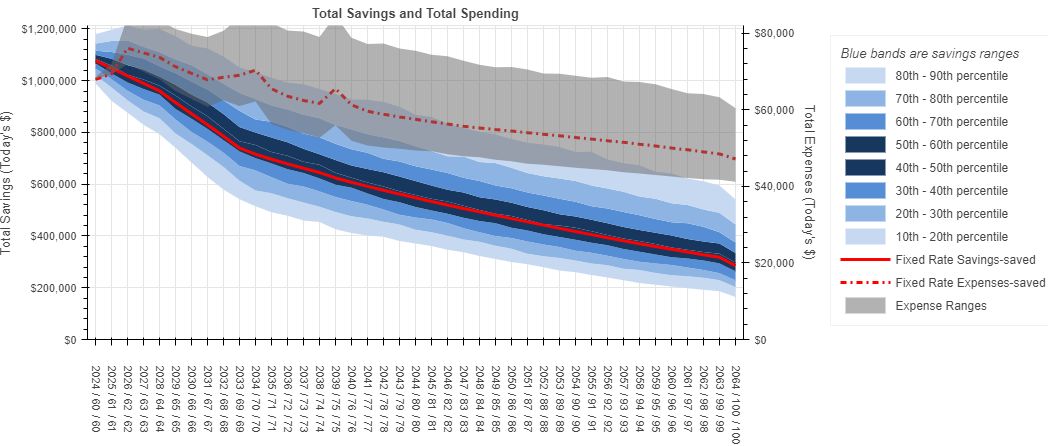

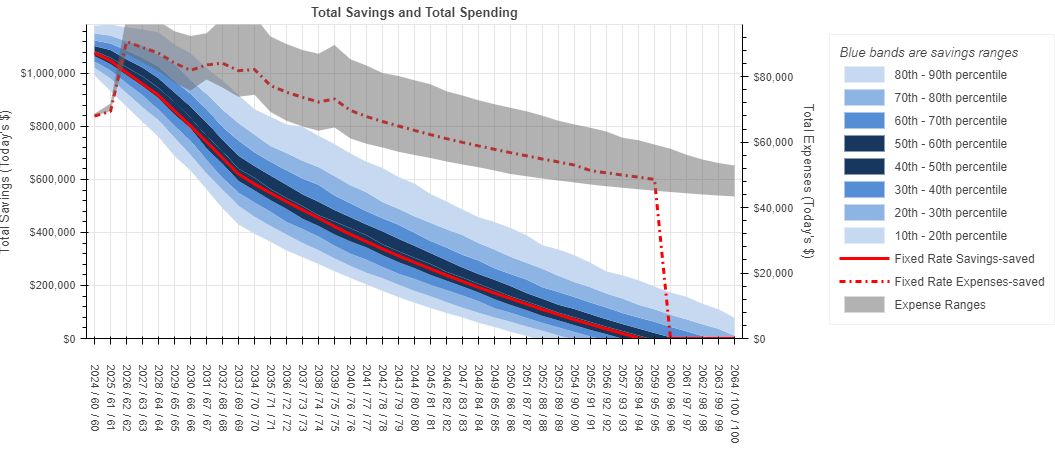

This page compares the results of the Monte Carlo or Historical analysis for each scenario for which you have run the analysis.

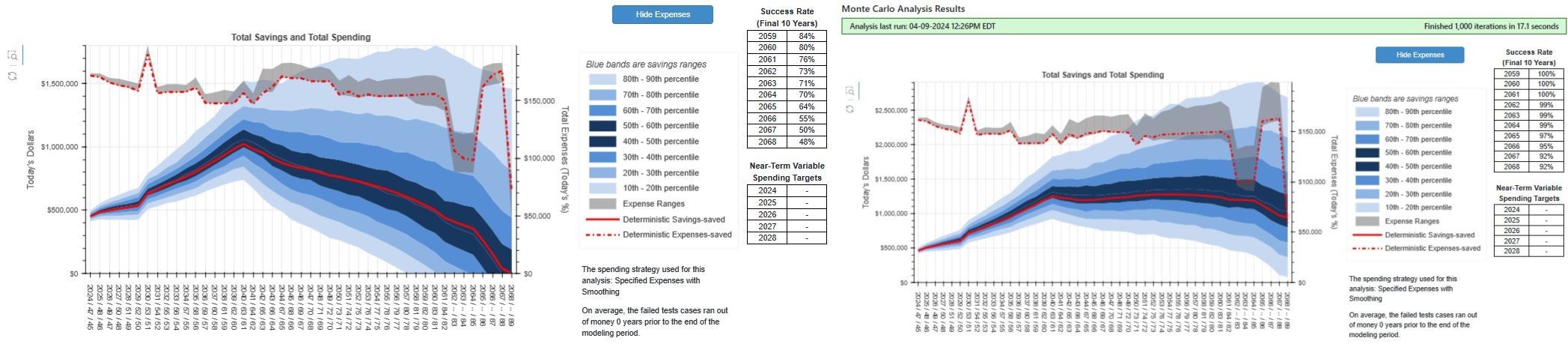

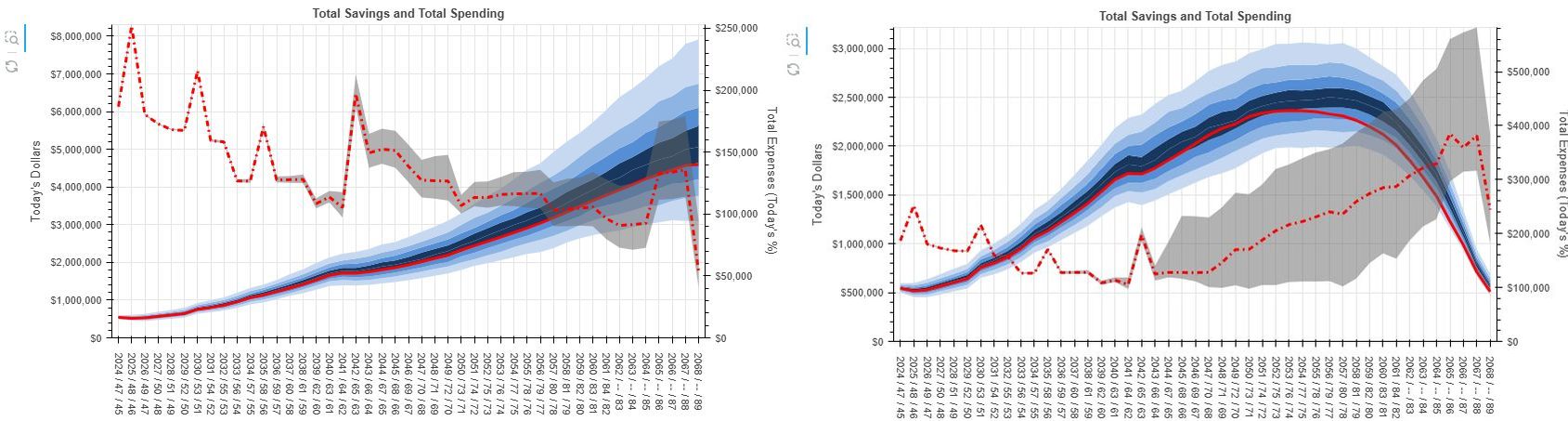

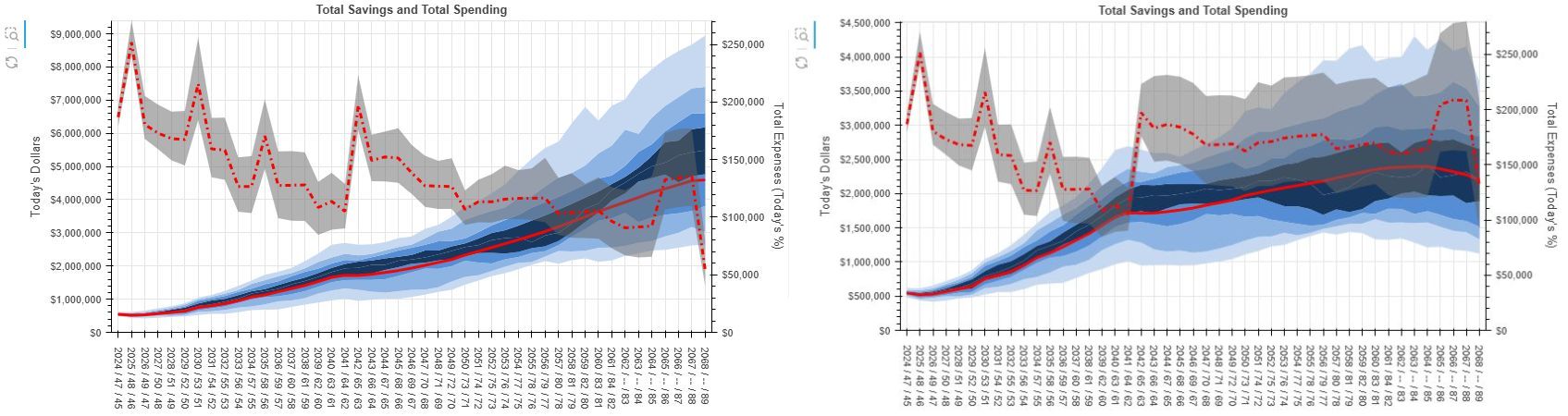

The graph shows the 10th and 90th percentile values from all three scenarios, color. The entire set of colored bands (like on the Run Analysis page) are not shown because the results from one scenario would obscure the results from the others. Here is the key to understanding this graph: the 10th and 90th percentile lines from a given scenario are of the same color and the space between them is all the blue bands shown on the Run Analysis page would be located. So, by comparing this “transparent” envelope from one scenario with that of another scenario, you can get a good sense of the relative success rates of those scenarios. With that said, this graph can display either savings or spending results as specified by the radio buttons at the top of the page. You may select to show the data in future or today’s dollars. Savings may be shown in effective or absolute dollars.

The table beneath the graph contains tabular success rates for the final 10 years of all three scenarios and variable spending for the next 5 years.

In the case of a scenario that models a shorter lifespan than the other scenarios, you will observe that the time axis extends beyond the death year and the savings and expense values drop to zero in those final years.

Things You Need to Know

The Welcome page (Home > Welcome) contains a quick overview of Pralana’s navigation, icons and links and various other things you need to know to use the site effectively.

Icons and Scenario Selection Control

Scenario Status

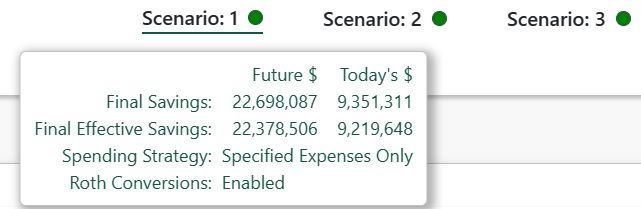

Almost every page shows the status of each scenario. By hovering your cursor over these icons, a pop-up box shows key information about the scenario. If the portfolio is in positive territory, the scenario icons will be green; otherwise, they will be red. The dots will appear to spin which the scenario is recalculating.

Pralana models up to three scenarios simultaneously but in most cases the inputs and outputs from only one of these scenarios will be visible at a time. You can select the active scenario via radio buttons like these:

.

.

Site Icons and Links

Below is the guide from the Welcome page:

Scenario Snapshot / Baseline

icon at the top of the page

to save a snapshot of the active scenario’s projections to ‘baseline’.

The baseline contains key results metrics, by year, for the scenario.

After setting the baseline, you may continue editing the scenario’s

inputs. To see how those edits have altered the scenario’s

projections, go to Review > Graphical Projections > Current vs

Baseline.

icon at the top of the page

to save a snapshot of the active scenario’s projections to ‘baseline’.

The baseline contains key results metrics, by year, for the scenario.

After setting the baseline, you may continue editing the scenario’s

inputs. To see how those edits have altered the scenario’s

projections, go to Review > Graphical Projections > Current vs

Baseline.Currently, Pralana saves only one snapshot/baseline of a scenario. When you set the baseline again, the baseline data is updated with the current scenario results.

Dynamic Number of Income, Expense, and Other Items

Pralana allows you to add and delete scenarios, income and expense items, asset classes, time periods, expense categories, and many other items. Each input form will display your current items and provide a “new” row or column through which you create additional items. To create a new item, just populate the “new” row or column, where the required inputs appear with a light blue background. Once those fields have been populated, the new item will immediately be added to the input form, the new label removed, and may continue filling in the remaining fields. To delete any line item, just click the red X at the right of the input’s row, (or bottom, if the fields are in a column).

The More > Resources > Max Number of Items page shows the maximum number of items you can define for each income, expense and other types of inputs. It also shows whether these inputs are plan-wide (apply to all scenarios), scenario-specific, property-specific, etc.

Pralana Supports a Single Browser Tab per User

Please be aware that Pralana supports only a single browser per user; if you create a duplicate tab in your browser and then attempt to access different views into Pralana simultaneously, you will encounter errors as it is not currently designed to support this mode of operation. Please refrain from this and restrict your usage to a single tab.

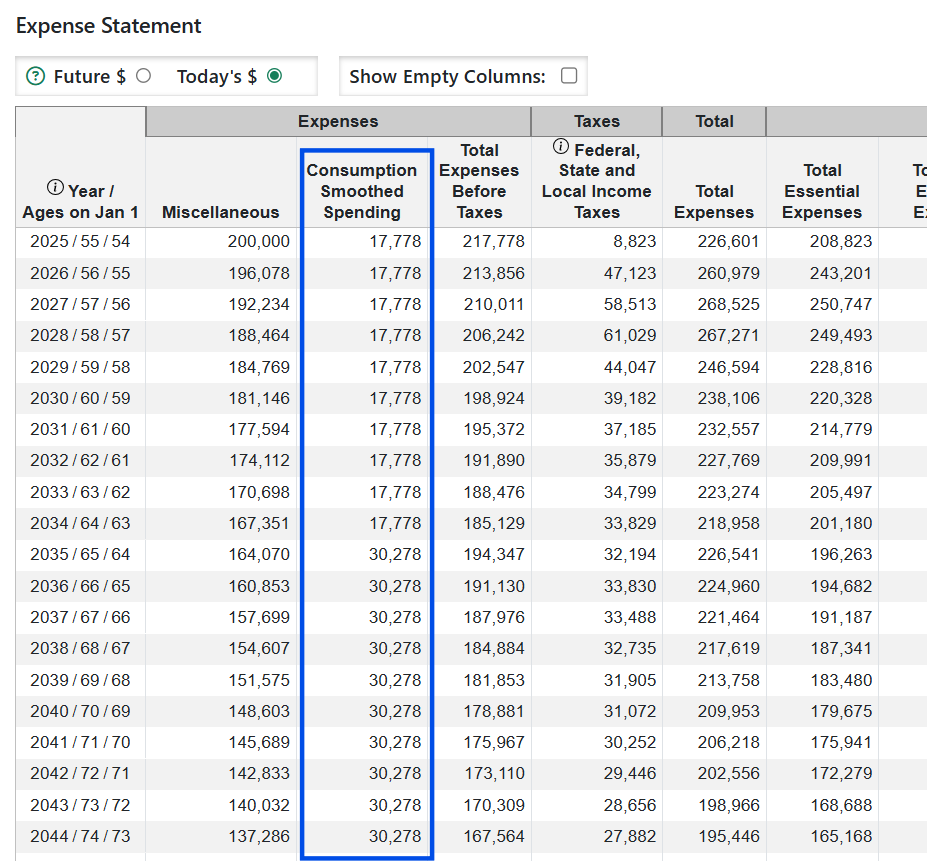

Tabular Projections

Pralana includes many tabular projections which are tables showing the projected values of metrics (in columns) by year (in rows). Tabular projections have these features:

Scenario selector: If your plan has more than one scenario, use this control to change the active scenario and update the tabular projection data.

Future $ or Today’s $ selector: You may select whether the values are shown in Future $ or Today’s $. See the “Future Dollars vs Today’s Dollars” below for more information.

Show Empty Columns: When checked Pralana will display all available columns, whether applicable or not. The default is to hide empty columns. Note: a few columns cannot be hidden including loan payments and interest on loan amortizations.

Compare to Scenario: Many tabular projections let you compare the active scenario to other scenarios, if your plan has more than one scenario. See the “Compare Scenario Metrics” section below.

Create PDF: Clicking this button will create a PDF of the tabular projection and open it in a new browser tab where you can view and download it.

Export to Excel: Clicking this button will export the tabular projection to Excel and prompt you to save the Excel file on your computer.

Column Heading Tooltips: Many column headings have an explanatory pop-up text box that will appear when you hover the cursor over the [i] symbol.

Gray First Row: For tabular projections that include account balances, property values, or loan balances, a gray row is shown at the top of the table to display the starting values as of December 31 of the year prior to your plan start year. This row serves as a reference and reflects the values you entered. All subsequent rows generally show year-end values. For example, if your first plan year is 2026, the balances shown in the 2026 row represent values as of December 31, 2026, after accounting for growth and any credits or debits during that year.

Totals Row: When displayed in Today’s $, most tabular projections will display a Total row at the bottom which will include totals for income, expenses, account growth and other metrics when meaningful. Totals are not shown for percentages (e.g. marginal tax rates) and end-of-year account balances, net worth, property values and loan balances.

The total row is never shown when viewing the table in Future $ because totals of Future $ are meaningless and misleading.

Example: You receive a $1million non-taxable windfall, in Future $ in 2026 in scenario 1 and in 2046 in scenario 2.

In Future $, the total windfall received is the same: $1million. But in Today’s $, the value received in 2026 is worth significantly more than the value received in 2046, reflecting the loss of purchasing power due to inflation over time.

Compare Scenario Metrics

When your plan includes multiple scenarios, certain tabular projection pages allow you to view results from two or three scenarios side-by-side. These pages will display a “Compare to Scenario” selector at the top. You can enable or disable other scenarios to add or remove their metrics from the table.

When additional scenarios are selected, Pralana prefixes each column with its scenario label (e.g., S1, S2, S3), as shown below. Values that differ from the first (baseline) scenario are highlighted visually.

If a comparison scenario differs from the first scenario, its values are highlighted with a yellow background.

If three scenarios are shown and all three values differ from each other, the third scenario’s values are highlighted with a blue background.

Small symbols (●, ◆) may also appear next to differing values to make differences easy to spot.

This visual formatting helps you quickly identify differences.

Future Dollars vs Today’s Dollars

Pralana enables you to view its tabular and graphical projections in terms of either future dollars or today’s dollars, as specified by radio buttons like this:

Pralana uses the term “today’s dollars”, but it is technically identical to the term “present value” of a future income, expense, or account balance. See Appendix 2 – Future vs Today’s $ for more.

Income Examples

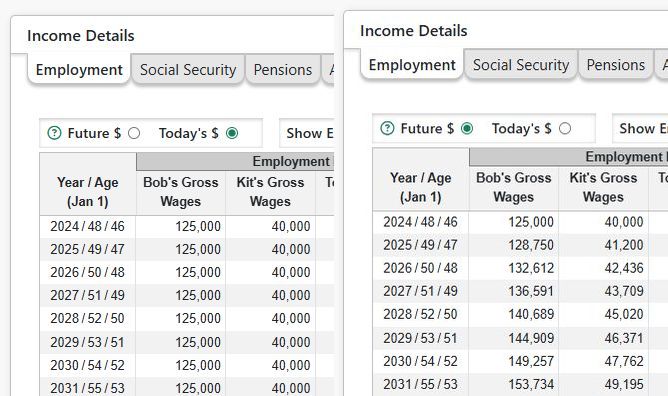

Now, let’s look at some income-related examples in Pralana. In the shot below, inflation is 3%. Bob earns $125,000 with a 3% annual COLA and Kit earns $40,000 with a 3% annual COLA. The shot on the left shows this in terms of today’s dollars and the shot on the right shows it in terms of future dollars. They have expenses of $75,000 that they expect to increase at the rate of inflation, or 3%. In terms of today’s dollars, both Bob’s and Kit’s incomes are flat and so are their annual expenses. Meanwhile, note that their Total Savings is increasing each year, thus signifying that its present value and its buying power is increasing each year.

Below is a similar example, except that in this case Kit has a fixed income with no annual adjustments. As you can see, in terms of today’s dollars her income is diminishing every year even though it is constant in terms of future dollars. This income stream is losing buying power every year. Meanwhile, Bob’s income is keeping up with inflation and maintaining its buying power.

Now, let’s take a look at a different example where Dick and Jane are retired and have no income. They do still have expenses, so they have a negative cash flow each year. The shot on the left shows their balance sheet in terms of today’s dollars, and the shot on the right shows their balance sheet in terms of future dollars. You can infer from this that the buying power of their savings is decreasing each year but that is not evident when looking only at the balance sheet on the right, thus illustrating the benefit of seeing the data in terms of today’s dollars, or its present value.

Expense Examples

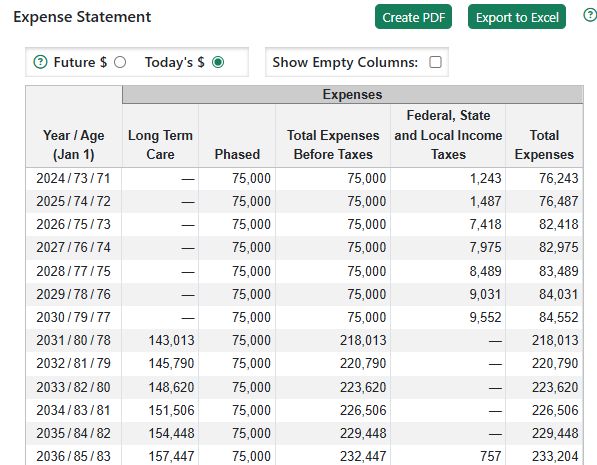

Now let’s look at some expense-related examples. In the shot below, you can see that general inflation is 3% and there are no add-on increases for healthcare, long-term care, college, etc. We have specified phased expenses of $75,000 starting in 2024 and LTC expenses of $125,000 starting in 2031. Here is a shot showing those projected expenses in terms of today’s dollars.

Now let’s include 2% LTC-specific inflation on top of general inflation, as you can see here:

Now let’s see what effect this has on the projection of expenses:

In contrast to the case with no LTC add-on inflation, this case does have some LTC add-on inflation and, therefore, LTC expenses are increasing in terms of today’s dollars while Phased expenses remain constant as in the prior example. This is the expected result of an expense that increases faster than the general inflation rate since that rate is the basis for converting future dollars into today’s dollars.

Unscheduled Withdrawals and Iterative Tax Calculations

Pralana performs detailed income tax calculations and includes those taxes in annual expenses which are subsequently used to determine annual cash flow. When that cash flow is negative, it results in a subsequent unscheduled transfer (i.e., a withdrawal) from one or more of the taxable savings, tax-deferred savings or Roth savings accounts, depending upon the withdrawal priorities specified by the user on the Financial Assets/Management page and the balances of those accounts.

Any such unscheduled transfers from tax-deferred accounts are a taxable event; however, the taxes for the year in question will have already been calculated and iterative tax calculations are required to properly determine the total taxes for this case. Pralana is designed to do these iterative calculations but that capability is not enabled in the releases to date. The reason for this is to enable direct comparisons to PRC2023 and PRC2024 (Excel) which do not perform iterative tax calculations. Consequently, for now, those transfers are treated as ordinary income in the next year, and that will be reflected in the next year’s AGI just as they are in the Excel tool.

Any such unscheduled transfer from taxable savings that results in long term capital gains is a taxable event and is handled the same as unscheduled transfers from tax-deferred savings.

Long term effects of this design simplification on the accuracy of Pralana’s projections have been studied and they are minimal; however, this may affect the optimization of Roth conversions in the near term.

Best Practice for Using Pralana

Pralana is a powerful and flexible planning tool, and it is best approached as an iterative process rather than a one-time exercise. This section provides a recommended workflow to help you build, analyze, and refine your plan without becoming overwhelmed. Some terms and features mentioned here are explained in more detail later in the manual; for now, focus on the overall progression. You can return to this section as your familiarity with the tool grows.

1. Start Simple with Quick Start

Begin by using Quick Start to create an initial version of your plan. Navigate to Build > Get Started > Quick Start and enter approximate information about your income, expenses, assets, and assumptions. At this stage, precision is not important—your goal is to establish a reasonable baseline.

After completing Quick Start, visit the Build > Income, Build > Expenses, and Build > Financial Assets pages to see how your inputs were translated into detailed entries. Then review the results on Review > Tabular Projections to gain a basic understanding of what the projections are showing.

2. Build Out the Details

Next, return to the Build pages and add more detail to your income sources, expenses, and assets. If you have not yet started Social Security, select start ages for yourself and your spouse—you can refine these later.

You may want to periodically set/update the baseline so you can see how changes affect the scenario results.

As you add detail, review the associated income or expense projection on the input page or return to Review > Tabular Projections to confirm that the overall results align with your expectations. At this stage, focus on understanding the deterministic projections before moving on to more advanced analyses.

3. Assess Risk with Monte Carlo Analysis

Once your deterministic results make sense, run a Monte Carlo analysis using the default assumptions. This analysis helps you understand the range of possible long-term outcomes and the likelihood that your plan remains viable.

If the projected success rate seems unacceptably low, consider adjustments such as:

Delaying retirement

Changing Social Security start ages

Reducing spending

Adding part-time work in retirement

Modifying your investment strategy

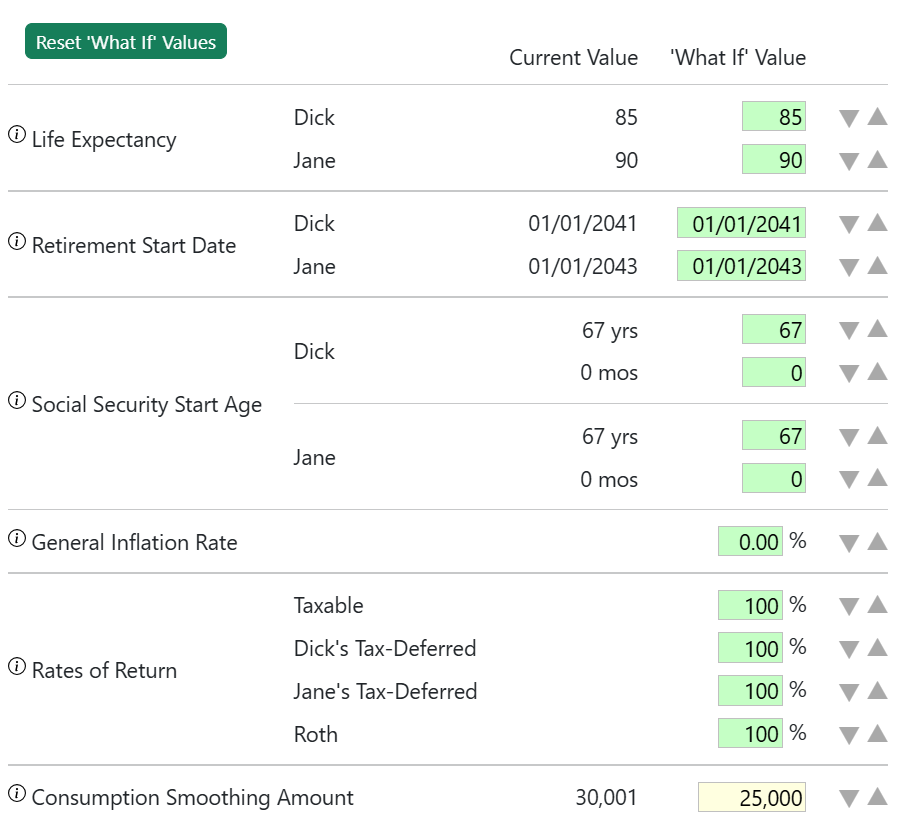

You can freely iterate between the Build, Review, and Analyze sections as needed. If desired, you can also explore different assumptions for market volatility directly on the Analyze > Monte Carlo Analysis page.

4. Explore Historical Outcomes

After reviewing Monte Carlo results, consider running a Historical analysis. This allows you to see how your plan would have performed under actual historical market and inflation conditions. You may also test specific historical sequences—such as starting in 1965, which represents one of the most challenging periods for retirees.

5. Optimize Key Decisions

With a viable plan in place, you can begin using Pralana’s optimization tools:

Social Security Optimization to evaluate alternative claiming strategies

Earliest Safe Retirement Date Analysis to determine when retirement becomes feasible with an acceptable probability of success

Variable Spending Strategies to model how discretionary spending might adjust in response to portfolio performance

Pralana supports up to three scenarios per plan, making it easy to compare strategies side by side.

6. Refine Tax and Roth Conversion Strategies

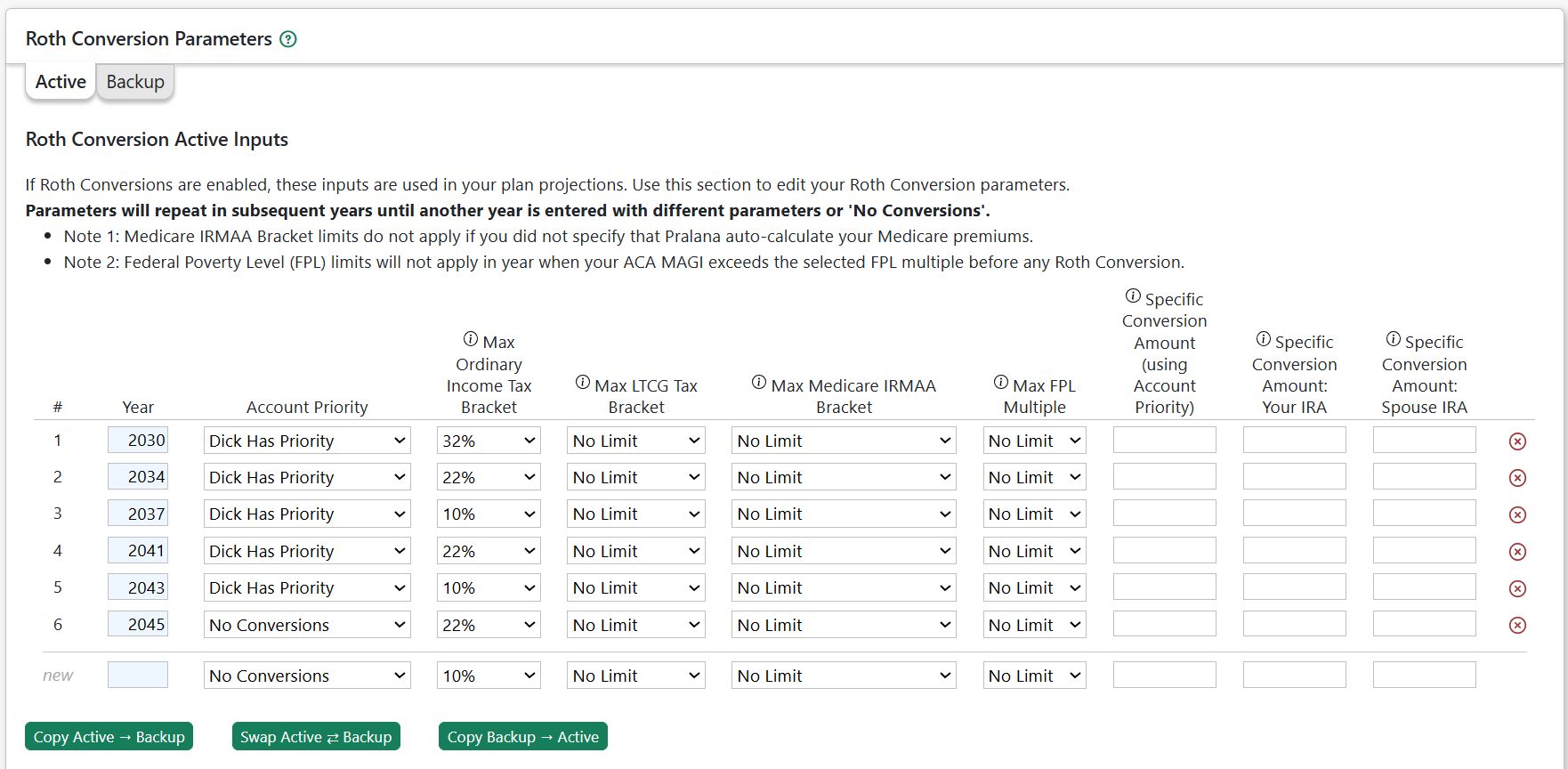

Roth conversion planning depends on many factors, including asset allocation, tax-deferred balances, tax brackets, ACA subsidies, and IRMAA thresholds. For this reason, it is generally best to explore Roth conversions after the rest of your plan is largely established.

Using Pralana’s Roth conversion tools, you can set constraints and allow the system to determine conversion amounts that seek to improve long-term after-tax outcomes. You may also specify specific conversion amounts, when needed.

7. Maintain and Revisit Your Plan

At this point, you have established a working plan. From here on, Pralana becomes an ongoing decision-support tool. As assumptions change, life events occur, or actual market returns replace estimates, you can revisit the Build pages, update your inputs, and re-run analyses to keep your plan current.

Updating your plan’s start year: See Appendix 1: How do I update my plan at the start of a new year? for tips on updating your plan at the start of each year. This information is also available in Pralana Online at More > Resources > FAQ and in the Pralana forum.

Structure and Navigation

Pralana is organized into several major, interrelated sections that are accessible from the fixed navigation bar at the top of every page. Depending on your subscription level, these sections include Advisors, Build, Review, Analyze, and More.

The Advisors section (available with a Platinum Pro subscription) enables financial advisors to create, manage, and maintain plans for multiple clients.

The My Plans section (available with a Platinum Family subscription) lets you see and manage multiple plans.

The Build section is where you create and modify your plans by entering assumptions, assets, income, expenses, and other inputs.

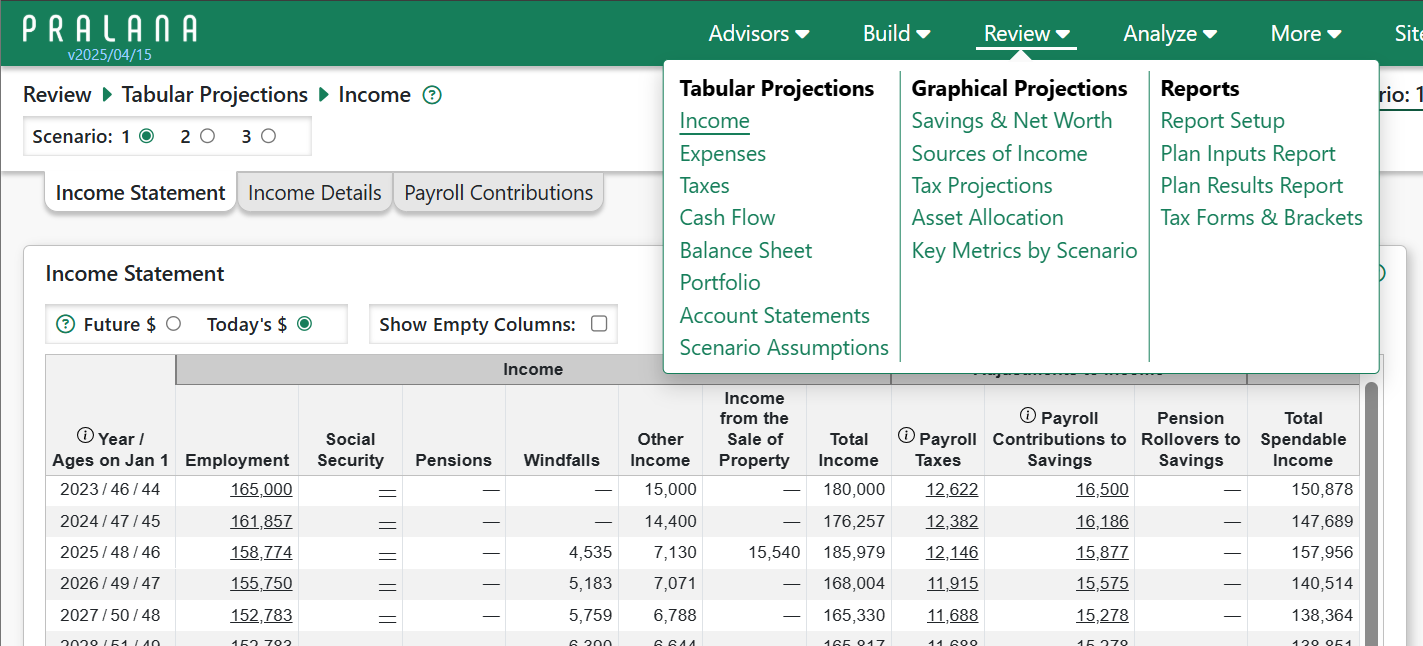

The Review section provides detailed outputs, including tabular projections and charts, and allows you to generate PDF reports and compare scenarios.

The Analyze section contains tools for analyzing and optimizing your plan, such as Monte Carlo and historical analyses, spending strategies, and optimization features.

The More section provides access to supporting information, including guidance on using the tool and release notes.

Hovering over top-level menu items reveals a submenu with links to related pages, organized by function, as illustrated in the screenshot below.

Advisors

The Advisors section contains two subsections:

Advisor Profile, where you can specify your name, certifications and contact information for Reports produced for your clients.

Client Plans, where you can add, manage and delete plans associated with multiple clients. Client Plans has a tab ‘Plan Adoption Log’ that shows the history of plans adopted by a client.

The Advisor link and subsections will only be visible to Platinum Pro users.

Home

The Home menu contains three pages:

Welcome: provides useful information for new subscriber about using Pralana and how to get started building their plan.

Features: shows key features of Pralana.

Dashboard: landing page when logging in. It contains summary information about your plan and scenarios as well as charts and tables showing various plan projections.

Build

The Build section is where you provide the detailed inputs to establish your financial plan, and it contains these subsections:

Get Started - Begin defining your financial plan:

Quick Start, My Family, Scenario Assumptions, Import PRC Excel Export File

Financial Assets - Identify your financial accounts, characterize your portfolio, and define personal and investment loans:

Management, Accounts, Portfolios, Scheduled Withdrawals, SEPPs, Personal Loans and Investment Loans

Income - Define your sources of income:

Employment, Pensions, Social Security, Windfalls, Annuities and Other Income

Expenses - Define your expenses:

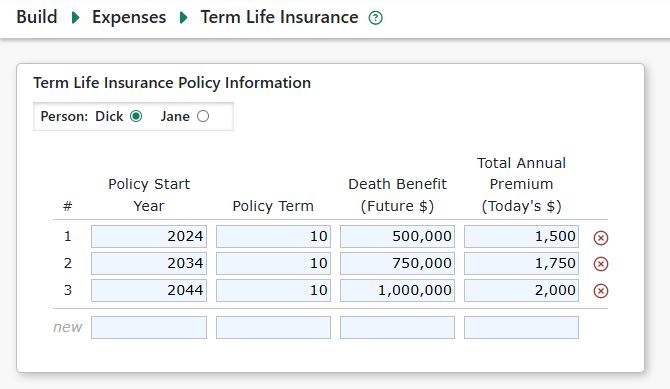

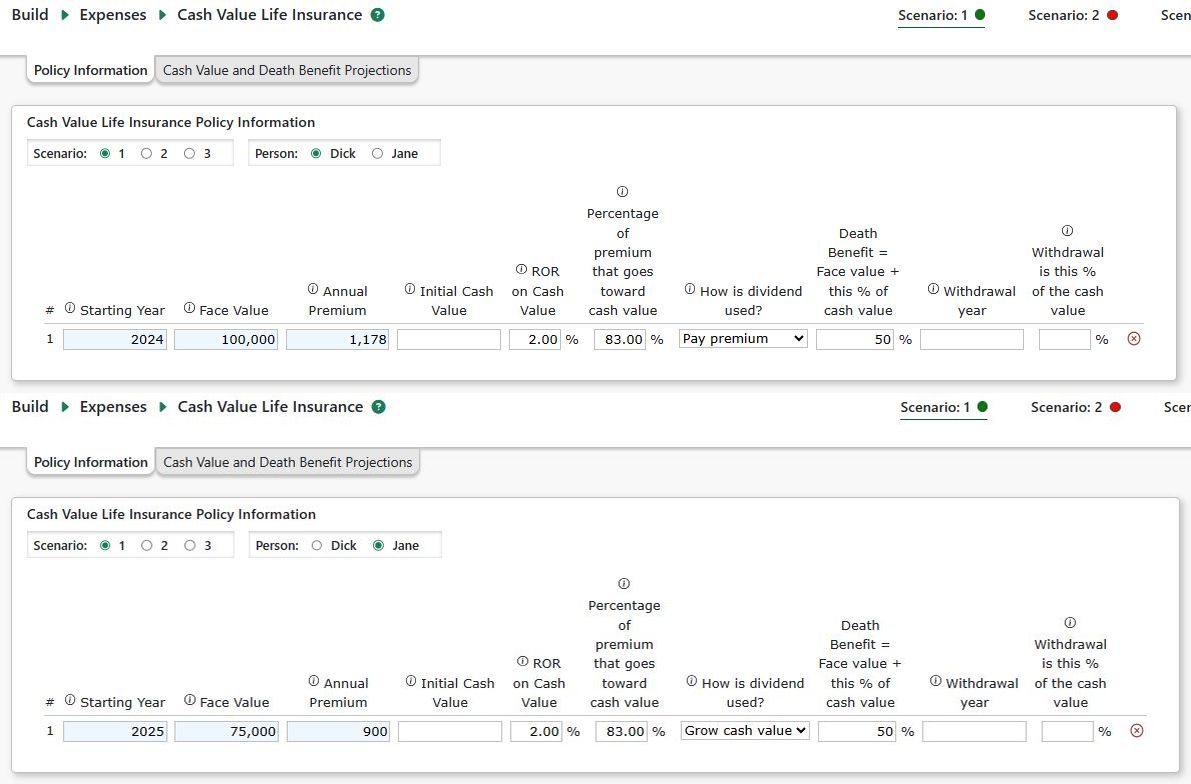

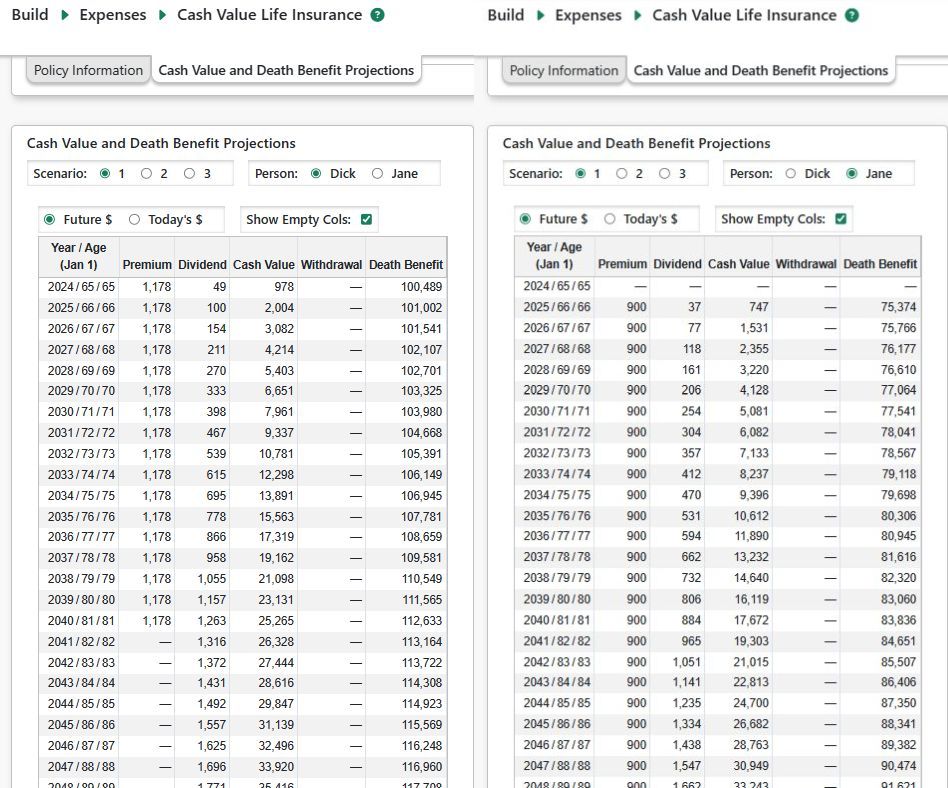

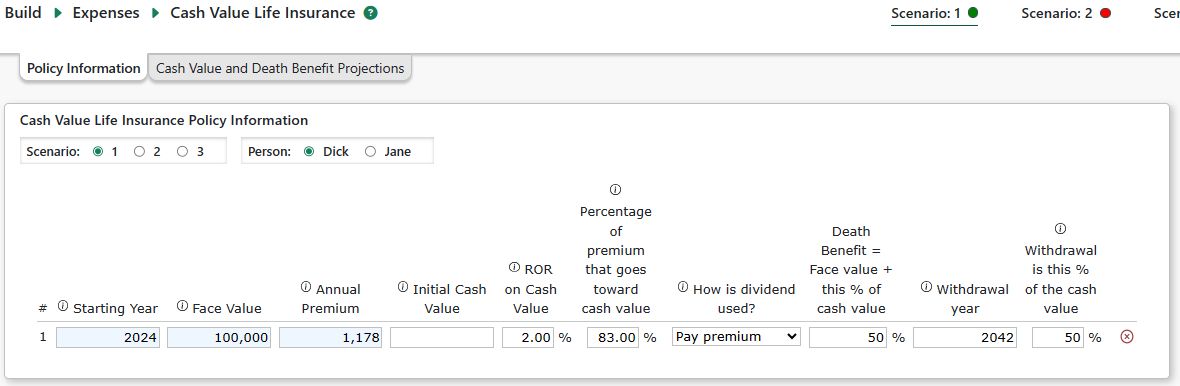

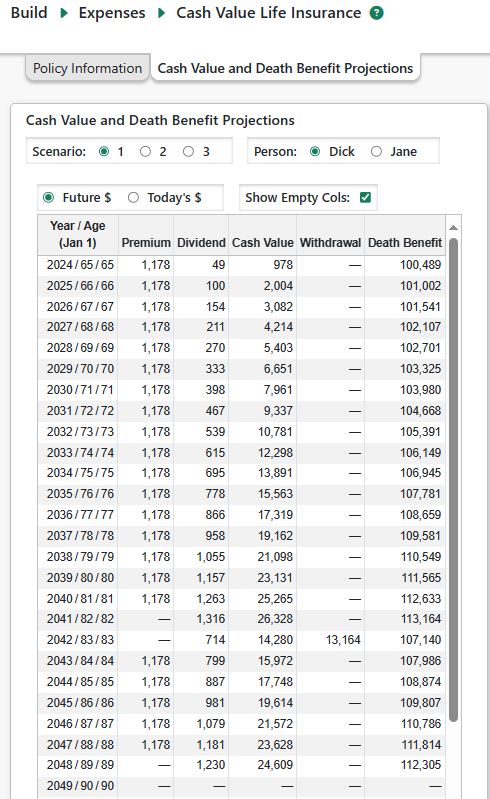

Personal Property, Rental Property, Children, Healthcare, Long-Term Care, Charity, Miscellaneous, Phased, Term Life Insurance and Cash Value Life Insurance

Review

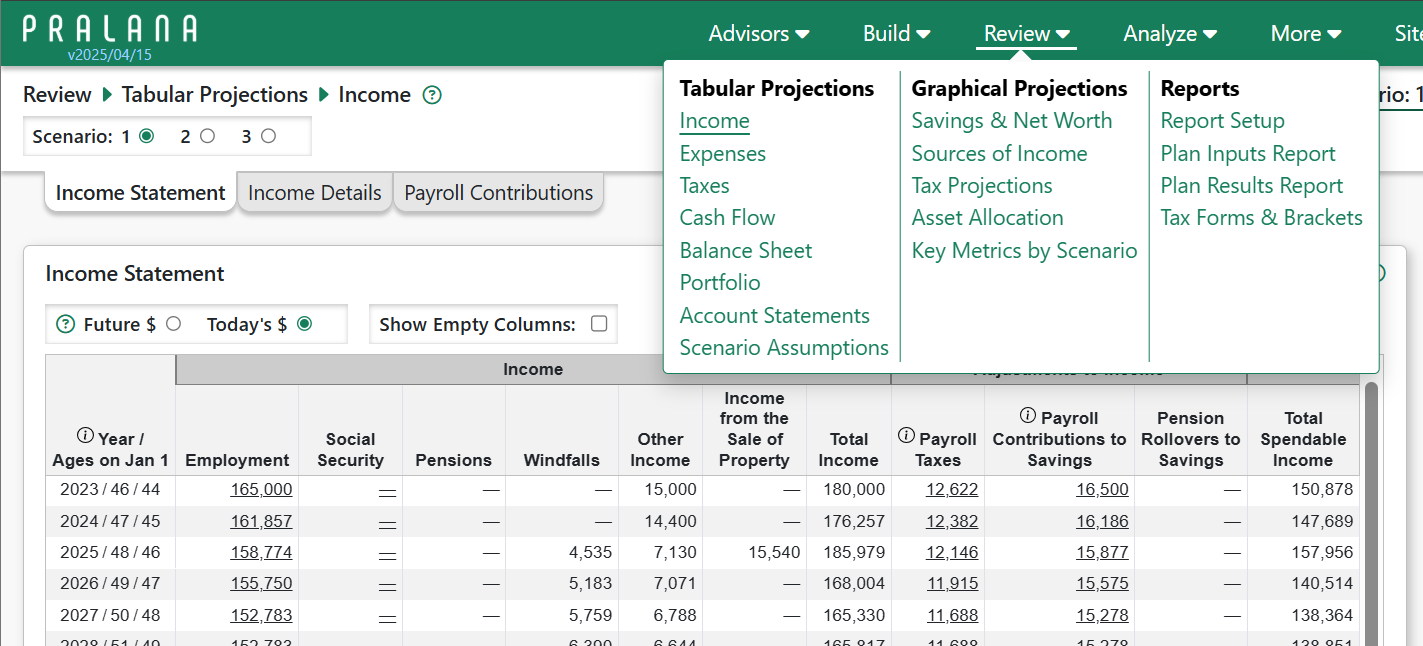

The Review menu contains these items that provide a detailed output of your financial plan:

Tabular Projections: detailed tabular projections for your scenario(s), including Income, Expense, Cash Flow statements, Balance Sheet and Tax Summary with many supporting tables.

Graphical Projections: charts showing projected savings and net worth, taxes and other graphical projections

Reports: Plan Inputs Report, Plan Results Report (both of which will create PDFs) as well as Tax Forms and related tax information.

Here is a screenshot of the Review pop-up menu:

Analyze

The Analyze section contains these subsections:

Monte Carlo Analysis: allows you to run and see the results of a Monte Carlo analysis of each scenario.

Historical Analysis: allows you to run and see the results of a Historical analysis of each scenario.

Spending Strategies: explore various alternate spending strategies, including Consumption Smoothing

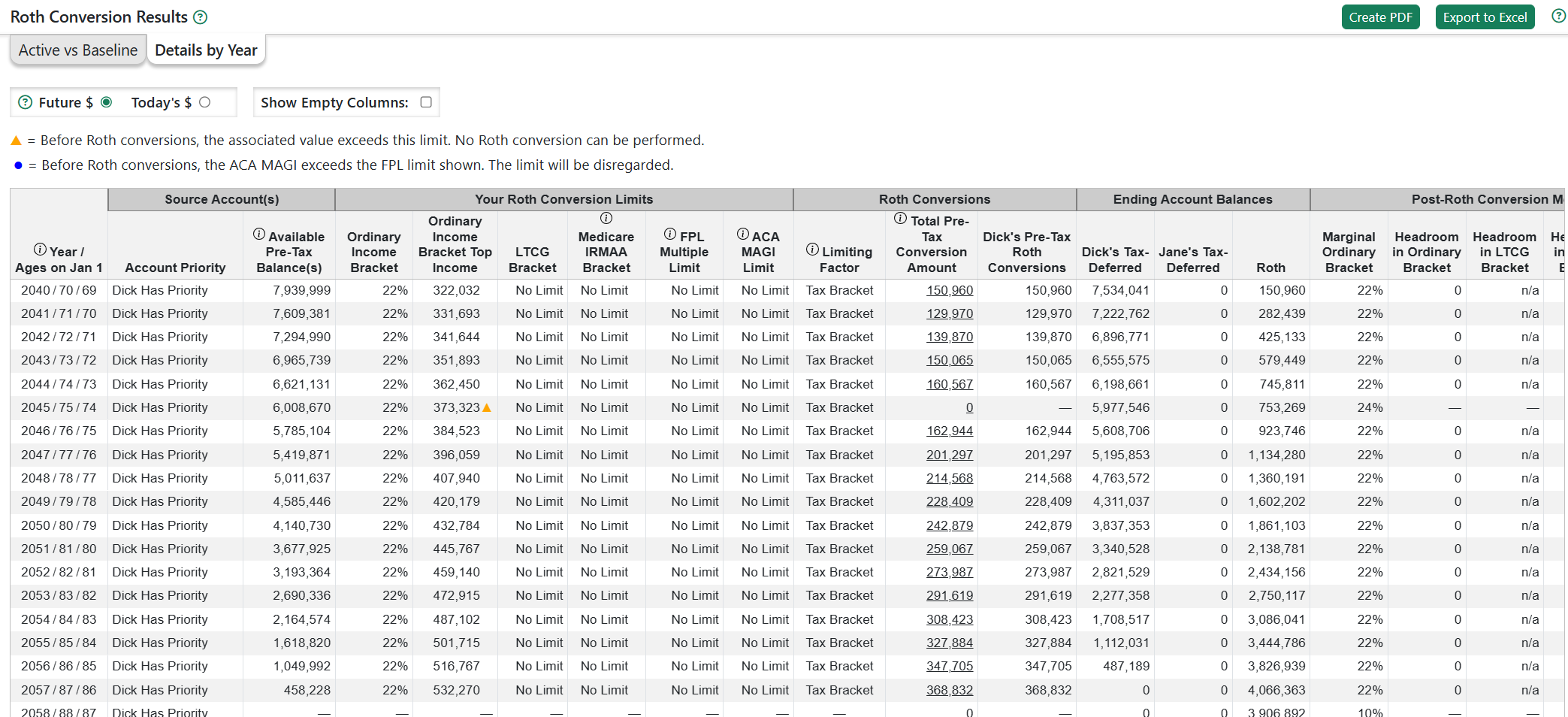

Roth Conversions: define and optimize Roth conversions.

Optimize Social Security Start Age: determine the optimum Social Security start age for yourself and, if married, a spouse.

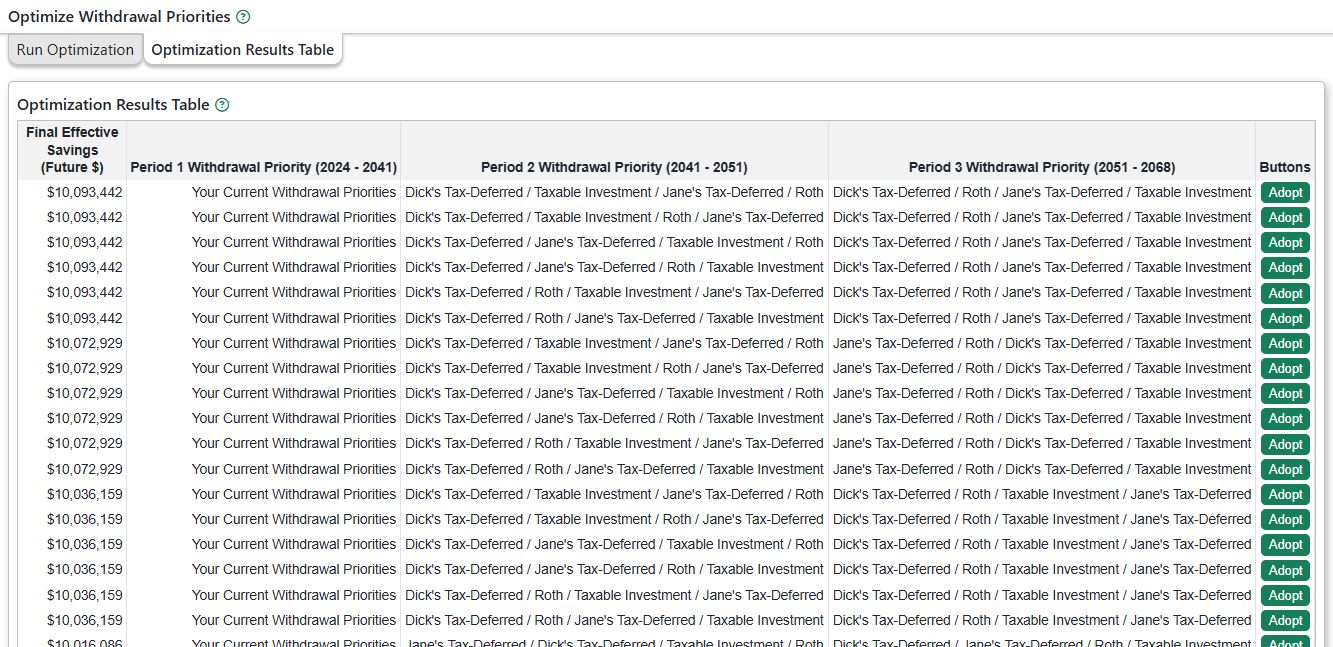

Optimize Withdrawal Priorities: an analysis to optimize withdrawal priorities among your various accounts when scenarios have cash shortages.

Earliest Safe Retirement Date: finds the earliest retirement date that yields a 90% probability that you will not outlive your money.

Here is a screenshot of the Analyze pop-up menu:

More

The More section contains links to other Pralana features which will evolve over time.

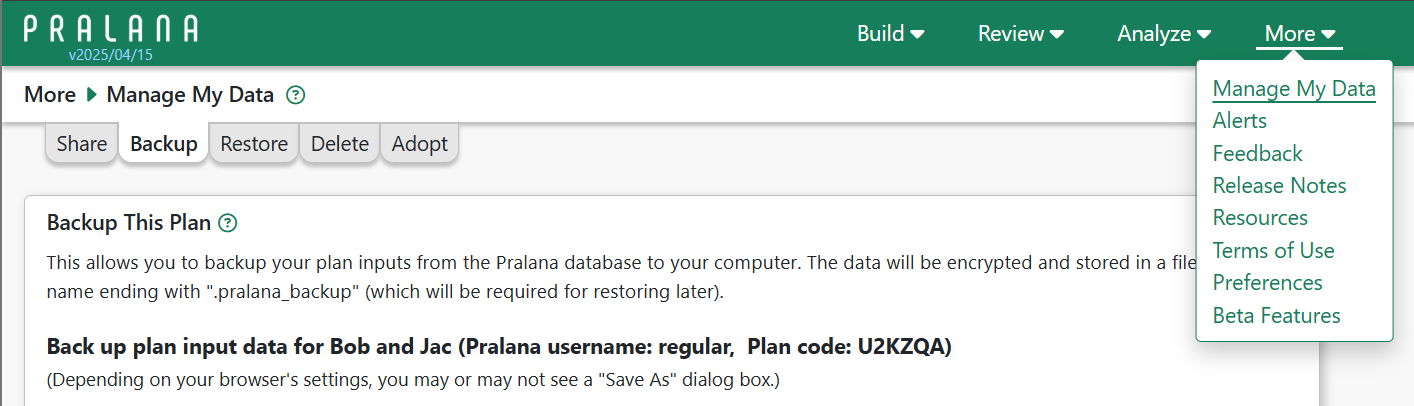

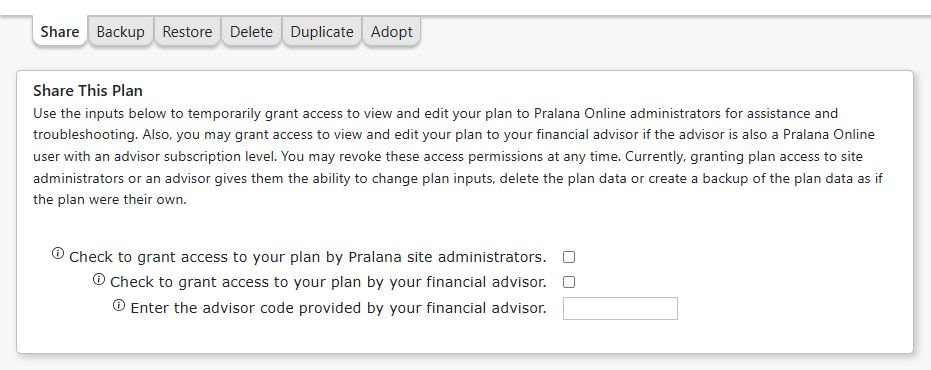

Manage My Data: provides access to features which allow you share your plan, backup, restore and delete your data from Pralana.

Alerts: shows various general site announcements and plan-specific messages generated by Pralana to make you aware of potential issues with your data. It may also contain information about known, unresolved bugs and site outages.

Feedback: shows your feedback and responses from the Pralana team

Release Notes: Shows recent past and pending future site change.

Resources pages for:

General Resources contains credits and acknowledgements as well as financial planning resources.

FAQ has answers to frequently asked questions.

How Do I… This section links to Appendix 1, providing brief explanations for common tasks and frequently asked questions about using Pralana.

PRC Excel vs Online summarizes differences between Pralana Gold (Excel) and Pralana Online.

Privacy Notice

Terms of Use

Other items such as site preferences and beta features.

Features in the More Menu

Manage My Data

Selecting Manage My Data from the More menu will take you to a page with six tabs, as shown here:

See the Data Security section for information about what data is provided to Pralana and how it is secured as well as best practices you can use to protect your data.

Backup This Plan

You may use this feature to extract and download your Pralana plan input data to your local computer. The downloaded file will be encrypted and may contain security measures to prevent unauthorized use by others or use in violation of the Pralana Terms of Use for your subscription level. The backup is intended for short term use. See notes on the Backup page and the limitations below in the Restore section, below.

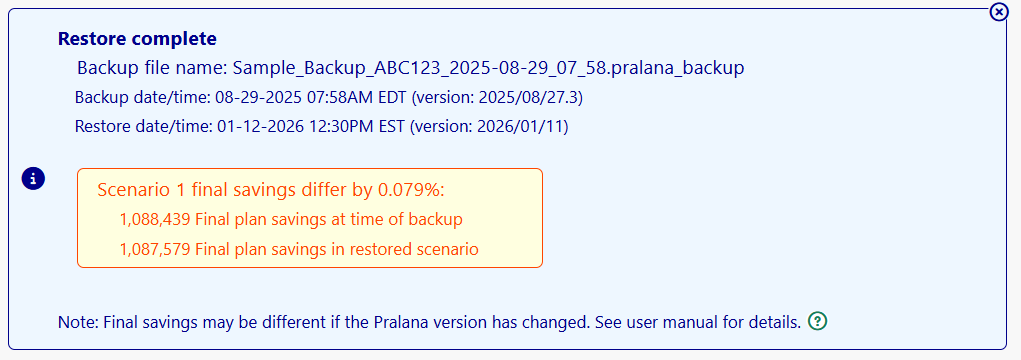

Restore Plan from Backup

You may use this feature to restore your Pralana plan using a previously downloaded Pralana backup file. We will make reasonable, best efforts to maintain backward compatibility for restoring backup files as Pralana is updated over time. The financial projections made by Pralana using a recovered backup file may differ from the projections made at the time the backup was made due to changes in tax parameters and changes to the calculations. You will be notified when restoring if the plan’s final year savings for each plan scenario match or differ from the corresponding amounts at the time the backup was created. See Appendix 4 – Restore from Backup Reference for more information about restoring from backup for the various subscription levels.

Delete This Plan

At any time, you may use the Delete feature to immediately, permanently and irrevocably remove your plan data from the Pralana database. Your plan inputs will be deleted and replaced with a generic plan for a fictitious ‘Dick’ and ‘Jane’. See the Data Security section for more information. You may request the site administrators delete your Pralana username/account by emailing us at mail@pralanaconsulting.com.

Duplicate This Plan

Applicable only to Pralana Pro users, the Duplicate function creates a new plan identical to the currently selected plan. This enables you to establish a “template plan” as a starting point for creating new client plans.

Adopt a Plan from Someone Else

The Adopt function enables you to adopt a plan created by another user, transferring ownership of that plan. For example, a financial advisor may create a plan for a client and then allow the client to adopt the plan. Or a person may create their own plan, then allow their financial advisor to adopt the plan (rather than temporarily sharing the plan). In either case, both client and advisor must have a Pralana subscription.

To adopt a plan, the current plan owner provides the plan code and a secret word to the recipient who enters that info on the Adopt page and simply clicks the ‘Adopt Plan’ button. While there are well over 1 billion possible plan codes, the secret word requirement adds an extra layer of security. The adoption process effectively changes the ownership of the plan and only the owner of a plan can delete that plan. Advisors can never own more plans than their Pralana subscription supports.

Important:

If the person adopting the plan is an individual user, the adopted plan will irrevocably replace the person’s existing. If the recipient is an advisor, adopting a plan will simply add the newly adopted plan to the advisor’s list of plans.

The existing owner of the plan will no longer have access to the plan, after it is adopted. If the existing owner is an individual user (not an advisor), a new plan with default inputs will be created for the existing owner.

The existing owner may choose to create a Pralana backup of the plan before providing the adoption information to the recipient. This back up may be later restored (see Restore for important information).

Tools

Compare Scenario Inputs

If you have at least 2 scenarios, this feature lets you compare the inputs between 2 of your scenarios. It will show you the categories of inputs that are the same and, if different, which items are different. Optionally, you may choose to see differences only. This is useful if the 2 scenarios were identical and you subsequently made changes. It highlights the changes.

Change Log

The Change Log shows the most recent edits to your plan. Use this to look back to see old and new values for each edit. The log will periodically be pruned to contain only the most recent 100 edits. Certain actions, such as restoring a plan from backup or copying or deleting a scenario may delete log items prior to that action.

Search Metrics

This feature allows you to do a keyword search of the column names in all tabular projections. The results will show a list of matching columns, with the associated Page Name, Column Name, and other useful information along with a link to that tabular projection.

Alerts

Pralana generates user alerts to make you aware of announcements from

the develop, announcements regarding the completion of imports from

Pralana Gold and any related import errors, and error conditions that

have been detected while running the model on your data. Whenever one or

more alerts, other than ‘Success’ (green) are present with, you will see

one of these icons

(‘Info’, ‘Warning’,

‘Error’) in the status bar. The color represents the highest alert

severity level, if there are multiple alerts. To access your alerts, you

can click that icon, or you can click “Alerts” in the More menu.

(‘Info’, ‘Warning’,

‘Error’) in the status bar. The color represents the highest alert

severity level, if there are multiple alerts. To access your alerts, you

can click that icon, or you can click “Alerts” in the More menu.

The Alerts page organizes alerts by category and within category by scenario, if applicable. As with the icon in the status bar, the color of the alert indicates the severity: green=success, blue=information, yellow/orange=warning, red=error. The categories are:

General alerts applicable to all users. Usually these announce new features or provide other important site news.

Plan alerts specific to your plan which may include:

Feedback alerts: Let you know one of your feedback items has been updated by the Pralana staff.

Import alerts: Give you information about an issue encountered when importing data from your PRC Gold export file.

Input alerts: Warn you about an issue with one of your inputs.

Calculation alerts: Warn you about an issue encountered when calculating your scenario projections.

Error alerts: Warn you about an error that has occurred.

Other alerts: Other types of alerts.

Most alerts first appear on either the applicable page or on all pages. You can dismiss alerts by clicking on the circled ‘x’ icon in the top right corner. Dismissed alerts will appear on the Alerts page where you can click the circled ‘x’ again to Delete Forever.

Some alerts will re-appear if the condition that created them occurs again. Other alerts will automatically disappear if the condition that created them no longer exists.

Many alerts that affect multiple scenarios and/or projection years will be listed once and the affected scenario(s) and/or year(s) will be listed in the body of the alert.

Feedback

Here you can see any feedback items you have created and the staff response. You may edit your feedback item to add an update or change the category or status. Currently, Pralana does not support adding pictures/screenshots to feedback items.

To create a new feedback item, use the Feedback link on the right side of the page header.

Release Notes

This page shows ‘pending’ and recent site changes.

Resources

This page contains useful information about Pralana for our subscribers. Content may be added or changed from time to time.

General Resources

Contains useful information and resources for Pralana subscribers as well as credits for third party data we may use.

FAQ

Contains the answers to frequently asked questions from our subscribers.

Max Number of Items Shows the maximum number of items you can define for each income, expense and other types of inputs. It also shows whether these inputs are plan-wide (apply to all scenarios), scenario-specific, property-specific, etc. ~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

How Do I…

Contains user manual links to commonly discussed retirement topics and how to address them in Pralana. This content is also included in Appendix 1 below.

PRC Excel vs Online

For subscribers of Pralana’s Excel-based products, this discusses some of the differences between PRC Excel and Pralana Online.

Feature Voting

Allows subscribers to cast up to 6 votes for a short list new features to help the Pralana team prioritize these features. There are many more feature and usability requests, not listed on this page, that may also be completed over time. Note: Feature Voting may be moved to the Tools page in an upcoming release.

Beta Features

This page may provide access to features for testing and feedback.

Getting Started

If you were a PRC2023 or PRC2024 Gold user, you can initialize Pralana by importing a PRC2023 or PRC2024 export file. To do that, go to the Build > Get Started > Import PRC Excel Export File page and click the button. That will bring up a dialog box where you can select that export file from one of the folders on your local computer. Click OK and the upload and import process will be initiated. A pop-up message will appear when it is finished. Once you dismiss that, you should be good to go. The Build pages and subpages are where you will find most of your imported data, so a good starting point would be to peruse those pages to see how your data is represented in Pralana. Once you become familiar with that, you can proceed to the Review pages to examine the tabular and graphical projections generated from your data with the deterministic analysis method. From there you can proceed to the Analyze pages to consider doing further analysis of your plan.

When you are ready to start working on your plan, you can just visit each of the links at the top of every page, moving from left to right, and enter your data. Start with your basic assumptions and then progress to the Build menu to specify your income, expenses, and financial assets. Once those have been entered, you can visit the Review pages to examine tabular and graphical projections generated with your data to see how your plan works going forward.

Quick Start

The Quick Start page is intended to minimize the intimidation factor for first-time Pralana users by making the entry of basic assumptions, financial assets, income, and expenses similar to those of a typical, free retirement calculator. Whatever you enter on the Quick Start page will be automatically populated into the normal Pralana input pages where you can elaborate them with additional detail when you are ready. This page just enables you to get started quickly and easily so you can see what Pralana does with your inputs and see the types of outputs it produces with your data.

So, if you are a first-time user of Pralana tools, we recommend making your initial data entry on this page, then perusing the various Build (Financial Assets, Income and Expenses) pages to see how your data appears, and then visit the Review pages. There, you can see the deterministic projections made with your data, including detailed breakdowns of your income, your expenses, the calculated taxes, and the account balances on a year-by-year basis, on both a tabular and a graphical basis.

As you are ready, you can then start adding more detail to elaborate your plan, and there will probably not be any further need for the Quick Start page, so you can just ignore it; however, its contents will automatically be updated to reflect your subsequent inputs via the normal Build pages.

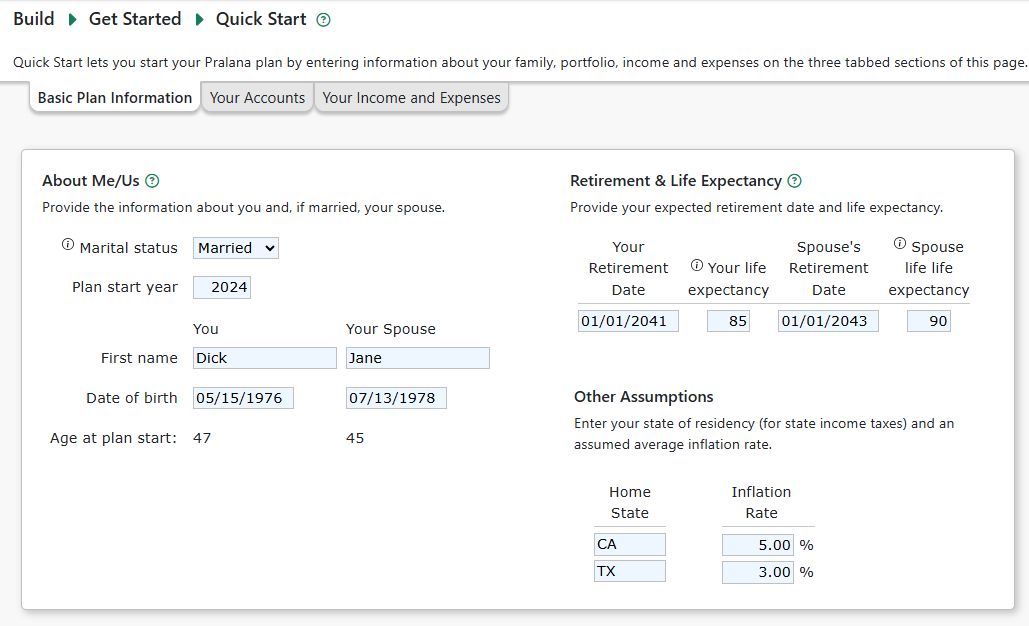

Basic Plan Information

Start by clicking the Basic Plan Information tab which will bring up a page with three simple sections, as shown below. In the About Me/Us tab, simply enter your marital status, your first name and your spouse’s first name (if applicable), your date(s) of birth. In the Retirement & Life Expectancy tab, enter the date you plan to retire from full-time employment and your life expectancy, and then do the same for your spouse, if applicable. In the Other Assumptions section, enter your state of residence and the expected inflation rate. Your inputs in this section will be replicated on the Build > Get Started > My Family and Scenario Assumptions pages.

Initial Account Balances

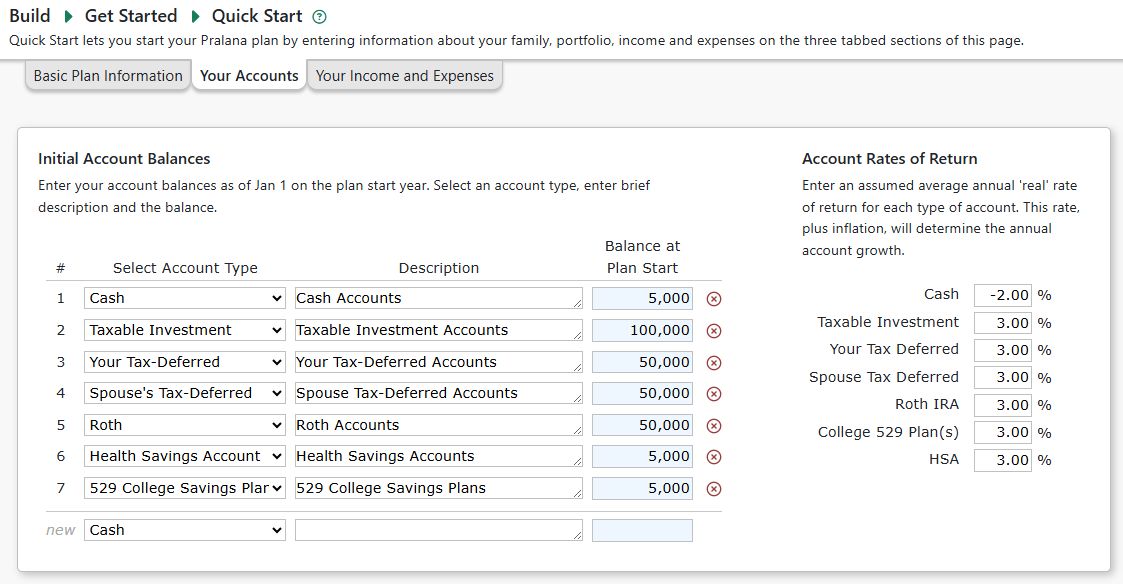

You can click on the Your Accounts tab to tell us about your accounts and their balances as of January 1 in the plan’s starting year. You can specify up to 10 accounts (cash, taxable investment, your tax-deferred, spouse tax-deferred, Roth, 529 college savings plan or health savings account) and for each of these you just need to give it a description and balance at the start of the plan. All the accounts within a given account type will be consolidated and modeled as one by Pralana and hereafter the term “account”refers to the consolidated accounts and not your actual accounts. Inherited accounts are modeled by Pralana, but they are not part of the Quick Start capability. Your inputs in this section will appear on the Build > Financial Assets > Account Initial Balances page. Here is an example:

Account Rates of Return

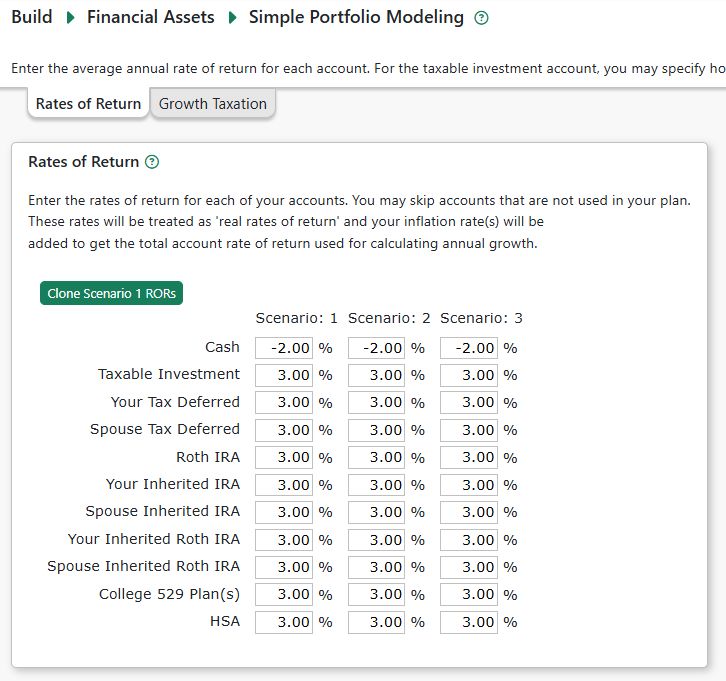

For each account type, you can then specify the expected average real rate of return (i.e., the return after inflation) in the fields to the right of the account balances fields. Your inputs in this section will appear on the Build > Financial Assets > Simple Portfolio Modeling page.

Your Income and Expenses

Finally, you can click on the Your Income and Expenses tab and define your employment, pension, and Social Security income streams, and your expenses. Windfall income, annuities, and Other sources of income are modeled by Pralana, but they are not part of the Quick Start capability. Likewise, property (personal and rental) expenses, Children’s expenses (including college educations and the associated funding), Healthcare expenses (including ACA and Medicare), are modeled by Pralana, but they are not part of the Quick Start capability. So, do not spend a lot of time trying to model these items accurately via the Quick Start page; maybe just enter some “placeholder” values. You will be able to model them in high fidelity when you are ready to move on to the primary Build pages (i.e., Financial Assets, Income, and Expenses).

Here is an example:

Quick Start Employment Income

You can specify multiple employment income streams for both you and your spouse. For each stream, you can specify the start/stop by either year or age. Then enter the annual amount in terms of today’s dollars and the annual increase amount. If you make contributions to a tax-deferred retirement plan, you can specify those here. Finally, if you receive company matching contributions to your tax-deferred retirement plan, you can also specify those here.

Your employment income inputs will appear on the Build > Income > Employment page. From there, you can add more detail regarding these income streams, if desired.

Quick Start Pension Income

You can specify multiple pension income streams for both you and your spouse. For each stream, you can specify the start by either year or age. Then enter the annual amount in terms of then-year (future year) dollars, along with the expected annual increase amount. Your pension income will appear on the Build > Income > Pension page. From there, you can add more detail regarding your pension income, if desired.

Quick Start Expenses

You can specify your expenses as line items in a simple table. Just enter the expense description, first year and last year (you can leave last year blank if the expense continues indefinitely), and amount in today’s dollars. Your expenses will appear on the Build > Expenses > Miscellaneous page.

My Family

This page contains two sections through which you introduce yourself and your family to the tool: About Me/Us and Children.

About Me/Us

The following items are global in nature and apply to all your scenarios.

Plan Start Year: Enter the year you wish the modeling to begin.

Marital Status: Specify your marital status via the pull-down menu.

Your First Name: Entering your name here will enable Pralana to include it in column headers to help you see the data that is unique to you.

Your Date of Birth: Enter your birthdate in the MM/DD/YYYY format.

Spouse’s First Name: This field will be hidden if a Marital Status of “Single” is selected. Entering your spouse’s name here will enable Pralana to include it in column headers to help you see the data that is unique to your spouse.

Spouse’s Date of Birth: This field will be hidden if a Marital Status of “Single” is selected. Enter spouse’s birthdate in the MM/DD/YYYY format.

Children and Other Dependents

This section allows you to enter your children and others for whom you provide support, their birth year (or the first year you will be providing support) and whether they are dependents for tax purposes.

For those you designate as a dependent for tax purposes, Pralana will, by default, assume tax dependent status for years in which the person is age 18 or younger -or- is in college and under age 24.

Children with gap year(s) between high school and college.

Children in college beyond age 23.

Disabled children or others who qualify as dependents for Federal tax purposes.

Notes:

The “Final Year as a Dependent” field is ignored if you do not check “Is this person a dependent for tax purposes?”

Persons who qualify as your dependents for Federal tax purposes will be assumed to also qualify as dependents for applicable state taxes.

Scenario Assumptions

The first section of this page allows you to specify your assumptions relative to inflation and how it will change over the modeling period.

Add/Delete Scenarios

On this page you can add up to a total of three independent scenarios, each of which has a complete set of assumptions, financial assets, income, and expenses. When you first start using Pralana it will only have one scenario and the active scenario will not be shown on the other input pages (because there’s only one scenario); however, as you add scenarios on this page, radio buttons will become visible on the other pages that enable you to select the scenario you wish to work on (i.e., the active scenario). When you first add a new scenario, it will be initialized to be identical to your first scenario (Scenario 1). You can also use this control to delete a scenario; however, Scenario 1 cannot ever be deleted.

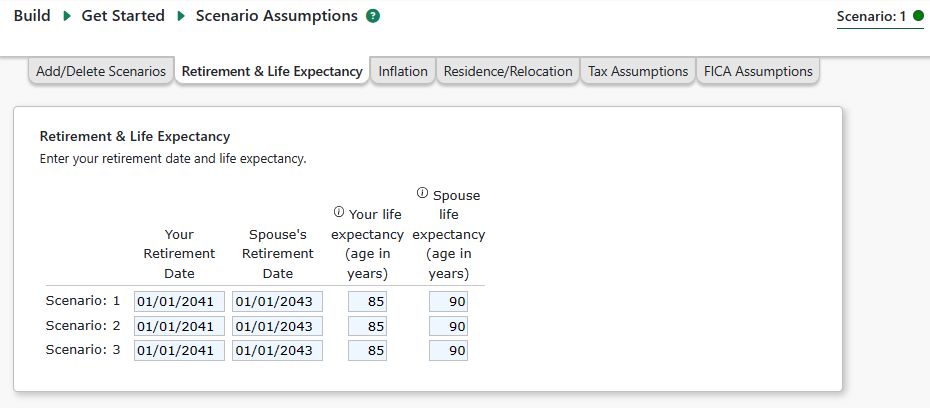

Retirement & Life Expectancy

On this page you can identify the date(s) on which you and your spouse plan to cease full-time employment, or your retirement date. Additionally, you can identify the life expectancy for you and your spouse. Pralana will assume you and your spouse die on the birthday on which the specified Life Expectancy is reached.

The retirement dates you specify here are used by Pralana in four ways:

It identifies the point in time where you MAY lose access to group health insurance premiums. This is used by the healthcare expenses page to assist in determining which time periods are applicable in your case.

It identifies the point in time where withdrawals from tax-deferred and Roth accounts become fair game for maximizing your standard of living and, hence, is used by Pralana’s consumption smoothing algorithm.

It identifies the point in time where non-essential spending (as explicitly specified on the Non-essential and Miscellaneous Expenses pages) can be replaced by variable spending based on your inputs on the Analyze > Spending Strategies page.

It can be used to identify the date on which most income streams can be started or stopped. If you enter the “wild card” character “R” in the start or stop field of an income stream, Pralana will use the retirement date specified here to start or stop that income stream.

If you have already stopped working full time, just enter January 1 of the starting year.

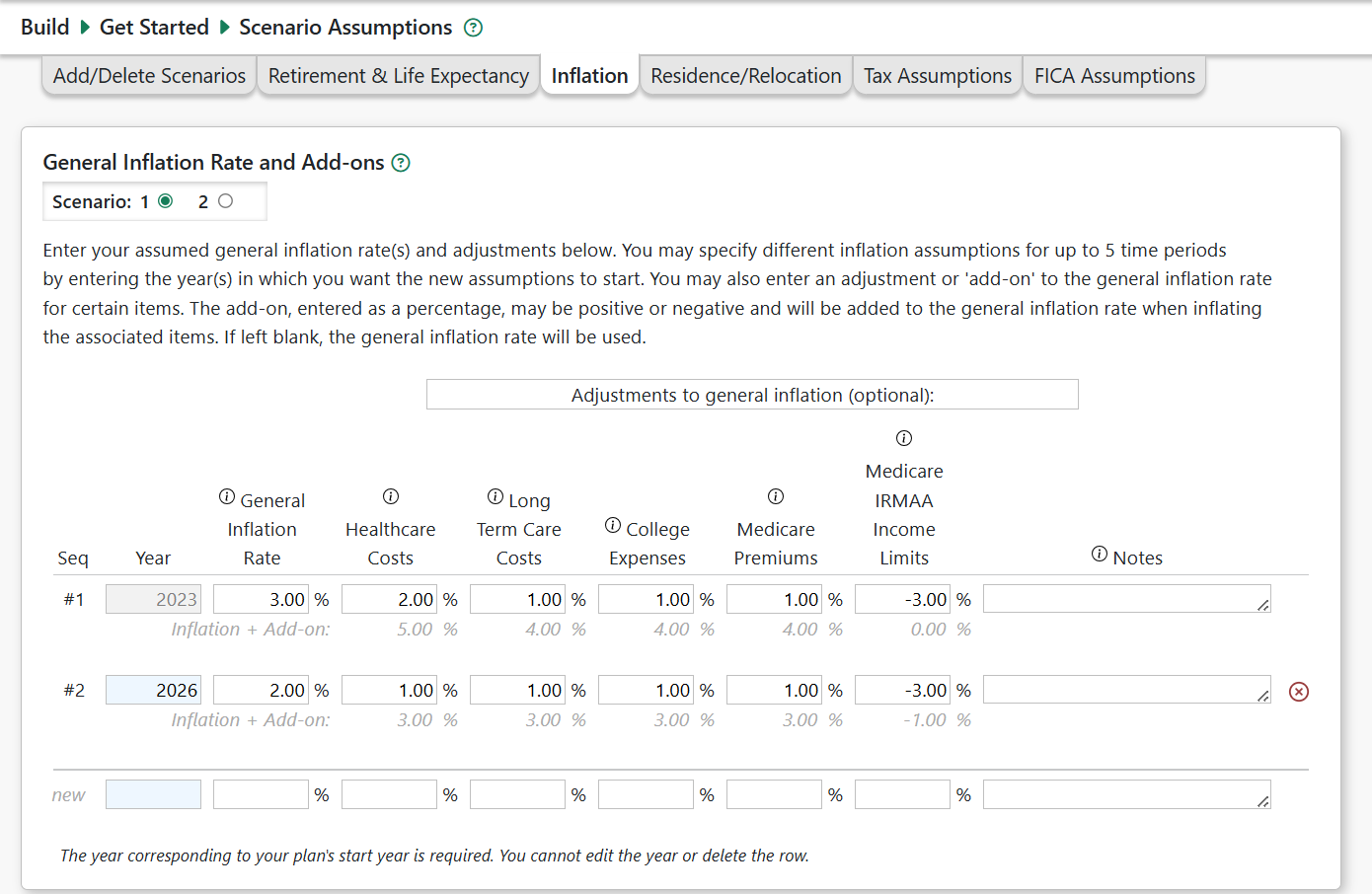

General Inflation Rate and Add-ons

On this page you can identify your assumptions about various forms of inflation, with different values for multiple different periods. Here is a screenshot:

General Inflation Rates

General Inflation Rate for Period 1: This is the general inflation rate that Pralana will use for deterministic calculations and Monte Carlo analyses. This rate will be in effect in the model’s starting year and will continue until and unless a different rate is specified for a second period.

General Inflation Rate for subsequent periods: If you wish to vary the inflation rate over the modeling period, you can do so by clicking entering the rate and start year for subsequent periods in the field labeled “New”.

Inflation Add-ons/Adjustments

You can also add some modifications to the General Inflation Rate. Below each add on, Pralana shows the total of your general rate plus the add-on applicable for that item. We may add additional inflation adjusters in the future.

Healthcare Costs: Healthcare costs will be inflated by the general inflation rate plus any adjustment that you enter here. You may want to factor in an increase in your own healthcare expenses as you get older. Leave blank if you think your healthcare costs will increase at the same rate as general inflation. Note: This adjustment does not affect Pralana’s calculated Medicare premiums which have a separate adjustment described below.

Long-Term Care (LTC) Insurance Costs: Long-term care expenses may be inflated by the general inflation rate plus any adjustment that you enter here. Note that for each long-term care expense you enter, you may choose whether to apply this LTC inflation add-on, your healthcare inflation add-on, or no inflation add-on.

College Expenses: College expenses will be inflated by the general inflation rate plus any adjustment that you enter here. Leave blank if you think college costs will increase at the same rate as general inflation.

Medicare Premiums: Medicare premiums are calculated by Pralana and will be inflated by the general inflation rate plus any adjustment that you enter here. Leave blank if you think Medicare premiums will increase at the same rate as general inflation. Note: This adjustment does not apply to annual insurance premiums and out-of-pocket expenses you enter on the Healthcare Expenses page. Use the Healthcare Costs inflation adjustment, above, for these.

Medicare IRMAA Income Limits: IRMAA income bracket limits will be inflated by the general inflation rate plus any adjustment you enter here. Enter a negative percentage if you think IRMAA income brackets will be inflated less than the general inflation rate, thus causing bracket creep over time.

Residence/Relocation

On this page you can identify your current state of residence and future plans to relocate to another state.

Year: The first row in the table is, by definition, your current state of residence and the year field will always be set to the model’s starting year. If you plan to relocate to a different state in the future, specify the year you plan to move in this field.

State: Pralana performs detailed state tax calculations for your state of residence, as specified here. This field contains a pull-down menu of the 2-letter state abbreviations, and you can just enter a blank if you live in a no-tax state.

Alternate State Tax Rate: State income taxes are particularly difficult to model, with 51 sets of rules (50 states plus the District of Columbia), so it is possible that the model is not always accurate for your case. Pralana state tax calculations ALWAYS use the standard deduction for your state, so that is one potential source of deviation between the model’s tax calculation and your actual taxes. If this algorithm does not seem to be calculating state taxes correctly for your case, you can use the alternative method provided on the Build > Get Started > Scenario Assumptions > Residence/Relocation page. Simply specify a rate that Pralana will multiply by the federal AGI to arrive at an estimate of your state income taxes. If you enter a value in this field, this alternative method will replace the detailed calculations.

Please note: If you do discover that Pralana is producing inaccurate values for the taxes in your state we will always welcome an email to provide us with the details so that we can continue to improve the model.

Local Tax Rate: This is the effective local tax rate in your geographical area. It will be multiplied by your Federal AGI to estimate your annual local taxes.

Tax Assumptions

OBBBA Summary

This page provides an overview of the July 2025 One Big Beautiful Bill Act. Pralana implemented these provisions in July 2025.

Federal Tax Law Settings

The enhanced Affordable Care Act (ACA) subsidies are set to expire at the end of 2025, meaning premiums will rise sharply starting in 2026 unless Congress acts to extend them.

What Are Enhanced ACA Subsidies?

These are expanded premium tax credits introduced in 2021 under the American Rescue Plan (ARP).

They were later extended through 2025 by the Inflation Reduction Act (IRA).

The enhancements made subsidies more generous and expanded eligibility to households earning above 400% of the federal poverty level (FPL)

Year Enhanced ACA Subsidies Expire: This field allows you to specify when Pralana should assume that enhanced ACA subsidies expire. You may set this to different values, by scenario, to see the impact on your ACA subsidies (for otherwise identical scenarios).

Federal Income Tax Rate Changes

Generally, Pralana assumes income tax bracket income limits and many other (but not all) Federal and state tax parameters will increase year-to-year using your general inflation rate. Some Federal and state tax parameters are not inflated. Inflating the ordinary income bracket income limits tends to avoid bracket creep due to income inflation.

Form 1040 line 15,

the Qualified Dividend and Capital Gains Worksheet lines 22 and 24, or

Schedule D Tax Worksheet lines 44 and 46

…as applicable in each tax year. Pralana’s Schedule D line 30 shows which tax calculation method is used.

The ordinary income tax brackets shown on Pralana’s Tax Brackets page are the published rates and will not include your adjustment(s).

FICA Payroll Tax Changes

Pralana can model future increase(s) in FICA payroll tax rates. Use this page to enter a percentage increase in the FICA payroll tax rate, starting in the year(s) you specify. Increase will be handled the same as described for federal income tax increases, describe above.

Import PRC Excel Export File

If you are PRC2023 or PRC2024 Gold user, you can initialize your Pralana plan by importing an export file from PRC2023 or PRC2024. To do this, just click the “Select and import your Pralana export.xlsx file”.

Modeling Your Income

Introduction to Income Modeling

Pralana enables you to model six categories of income as described below.

Options for Defining the Start and Stop of Income Streams

Pralana allows you to start and stop most income streams using any combination of four different methods to improve the fidelity of its modeling of partial-year income streams:

Age: If you specify an age, the income stream will start (or end) on the date the owner reaches this age (i.e., on his or her birthday).

Year: If you specify a year, the income stream will start (or end) on January 1 of this year.

Specific date: The income stream will start (or end) on this specific date.

Your (or your spouse’s) retirement date: If you enter an “R”, the income stream will start (or end) on the date specified in the “Retirement Date” field on the Build > Scenario Assumptions > Retirement Date/Life Expectancy page. This gives you the option to end an employment income stream and begin a pension income stream and even a post-employment income stream on the same date without literally having to enter that date multiple times. This, then, enables you to do what-if studies with your retirement date without having to go back and change the date in multiple locations. Further, this feature enables sensitivity studies around your retirement date on the modified Analyze > Sensitivities page.

NOTE: Pralana will start and stop your income streams at the beginning of the specified dates. If you want one stream to end and then another to start without a short loss of income in between, then you should set the stop and start dates the same. If you stop one stream on March 31 and begin the next one on April 1, there will be a one-day period where your income goes to zero in between these two income streams.

How Birthdays Affect Income Streams

Pralana enables you to start and/or end income streams based on your age to model partial-year income streams, and the convention is that age-related income streams begin and end on the birthday of the owner. As a quick example, let’s say your birthday is on July 1 and you plan to stop working when you’re 62 and start your pension when you’re 62. You would set the stop age of your employment income stream to 62 and the start age of your pension to 62. When you examine your income profile, you will notice half a year of employment income and half a year of pension income in the year in which you turn 62.

Another example is that of a married couple where both you and your spouse have your own Social Security benefits but your benefits are the higher of the two. If you die before your spouse does, your spouse will (in effect) get your benefits rather than his/her own during the “survivor” years. In the year in which you die, Pralana will model the Social Security income stream to accurately reflect both your and your spouse’s benefits up to the point of your death and then only your spouse’s survivor benefits thereafter.

A final example relates to the final year of the last-surviving spouse. If that person dies sometime during the year (as opposed to January 1), then only a partial year of income will be modeled in that final year.

Annual Inflation Adjustments

You can specify whether each income stream is adjusted annually in either real or nominal terms. If you specify “real”, then inflation will be added to the value you enter and this enables you to do what-if studies of the effects of different inflation profiles without having to come back to the Build > Income pages to make adjustments to the way each income stream is adjusted annually. If you specify “nominal”, Pralana will use the exact value specified to make annual income adjustments and these will not vary as a function of inflation.

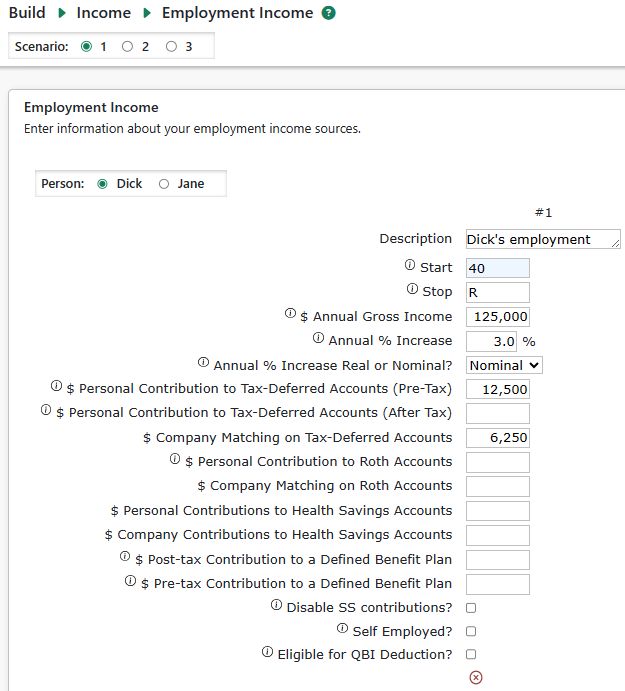

Employment Income

Inputs

You can define multiple employment income streams in this section and

they can be associated with either you or your spouse based on the radio

button at the top of the section. At any time, all streams associated

with the selected person will be visible. To create a new stream, just

populate the “new” column. When you do that, another “new” column will

appear to enable you to add the next stream if desired. To delete a

stream, just click the  at the bottom of the column.

at the bottom of the column.

Start and Stop: These fields enable you to specify exactly when the income stream begins and ends. You can enter an age, a year, a date (mm/dd/yyyy) or an R (for Retirement date). You can specify the start and stop fields by different methods and if the stop field is left blank the income stream will continue to the end of the modeling period. The income stream will not be modeled if the start field is left blank.

$Annual Gross Income: The annual income in terms of today’s dollars.

Annual Percent Increase: The annual rate of increase, and it can be real or nominal. If real, the income stream will increase at the rate of inflation plus the specified real percentage increase; otherwise, the income stream will increase at the specified nominal rate.

Annual Increases are Nominal? Check this box if annual increases are specified in nominal amounts (i.e., the specified value includes inflation). If not checked, the annual increases are assumed to be Real and the income stream will increase annually at the rate specified + general inflation. An advantage of specifying annual increases in terms of real amounts is that it enables you to investigate the effects of different inflation profiles without having to come back here and modify the rate of change of your income.

$ Personal Contribution to Tax-Deferred Accounts (Pre-Tax): The dollar amount to be deducted from this income stream that you or your spouse plans to contribute to a tax-deferred retirement plan on a pre-tax basis. Taxes on this income and all associated growth will be deferred until withdrawn. It is possible to specify contributions to tax-deferred savings without the owner having any earned income. If it turns out that total contributions exceed total income, the spendable income will be a negative number.

$ Personal Contribution to Tax-Deferred Accounts (After Tax): The dollar amount to be deducted from this income stream that you or your spouse plans to contribute to a tax-deferred retirement plan on an after-tax basis. These contributions will grow tax-deferred until withdrawn and they can be rolled over to a Roth IRA after retirement.

$ Company Matching on Tax-Deferred Accounts: The dollar amount that your employer or your spouse’s employer will contribute to your tax-deferred retirement plan.

$ Personal Contribution to Roth Accounts: The dollar amount to be deducted from this income stream that you or your spouse plans to contribute to either a Roth IRA or a Roth 401k. Taxes on this amount of income will be due in the year the income is earned.

$ Company Matching on Roth Accounts: The dollar amount that your employer or your spouse’s employer will contribute to your Roth accounts.

$ Personal Contribution to Health Savings Accounts: The dollar amount to be deducted from this income stream that you or your spouse plans to contribute to an HSA. Taxes on this income and all associated growth will be deferred. You can go to the Scheduled Withdrawals Table on the Financial Management/Management page to model qualified withdrawals from the HSA and these will be excluded from your AGI.

$ Company Contribution to Health Savings Accounts: The dollar amount that your employer or your spouse’s employer plans to contribute to an HSA on your behalf. Taxes on this income and all associated growth will be deferred. You can go to the Scheduled Withdrawals Table on the Financial Management/Management page to model qualified withdrawals from the HSA and these will be excluded from your AGI.

$ Post-tax Income Contributed to a Defined Benefit Plan: You can use this field to specify the size of your contribution to a defined benefit pension plan with post-tax dollars. The funds will come from your after-tax income and will not be contributed to any savings. Rather, they are assumed to help fund your Defined Benefit Pension detailed in the pension section of the Income page.

$ Pre-tax Income Contributed to a Defined Benefit Plan: You can use this field to specify the size of your contribution to a defined benefit pension plan with pre-tax dollars. This will be treated like a 401k contribution in that it reduces Adjusted Gross Income but has no effect on FICA; however, the funds on this line will not be contributed to any savings. Rather, they are assumed to help fund your Defined Benefit Pension detailed in the pension section of the Income page.

$ Payroll Deductions for Healthcare Insurance Premiums (Pre-Tax): Enter the amount of any pre-tax deductions for healthcare insurance premiums and other healthcare-related expenses. This amount will reduce taxable wages, but will not be deductible on Schedule A, Medical and Dental Expenses, to avoid two deductions for the same expense. Be sure not to include healthcare-related payroll deductions here and on the Healthcare Expenses page to avoid double-counting.

$ Other Payroll Deductions (Pre-Tax): Enter the amount of any other pre-tax payroll deductions, such as for commuter expenses. This amount will reduce taxable wages.

Disable SS contributions?: This control enables you to specify that this income stream is not subject to Social Security taxes.

Self Employed?: Check this box to indicate that this income is subject to self-employment taxes. Pralana will calculate the additional payroll deductions needed to cover the employer’s portion of payroll taxes.

Also, on the Healthcare Expenses page you may enter the percentage of your healthcare insurance premium expense that qualifies for the self-employment health insurance deduction, up to the amount of your self-employment income. The health insurance deduction will be included on Form 1040 Schedule 1, line 17 as an adjustment (reduction) to income. Also, your QBI deduction will also be reduced by 20% of this amount while the TCJA of 2017 tax law remains in effect.

Eligible for QBI Deduction?: Check this box if this income is eligible for the QBI deduction under the TCJA of 2017. Typically, this only applies to self-employment income but Pralana does not verify that this is self-employment income when applying this deduction.

Contributions to Savings

Pralana allows you to specify contributions to tax-deferred and tax-free savings but it does NOT provide any way for you to specify contributions to your regular investment account. Instead, contributions to regular/taxable accounts will always be calculated based on the difference between income and expenses. This is a major element of the Pralana design philosophy to ensure that all money is fully accounted for while accommodating ebbs and flows of both income and expenses. You can read more about this in the section on Modeling Your Accounts.

Income Projection

This tab shows the calculated Employment Income projection over your scenario years.

Pension Income

Inputs

Pralana allows you to define income from pensions, including pensions that include roll-overs to a traditional IRA and/or a Roth IRA. You can also specify survivor benefits, if any, as well as a Certain and Continuous period of a specified duration.

Each pension will be associated with you or your spouse based on the radio button at the top of the page. To create a new stream, just populate the “new” column. When you do that, another “new” column will appear to enable you to add the next stream if desired.

User Description: This is the field directly beneath the Pension# label that enables you to specify a textual description of the pensions. As always, create a blank by using the DELETE key.

Start and Stop: These fields enable you to specify exactly when the income stream begins and ends. You can enter an age, a year, a date (mm/dd/yyyy) or an R (for Retirement date). You can specify the start and stop fields by different methods and if the stop field is left blank the income stream will continue to the end of the modeling period. The income stream will not be modeled if the start field is left blank. If you want to model a lump sum pension, just set the start and stop to the same value.

Annual Taxable Amount: Enter this in future-year dollars. You can use the converter if your pension is specified in terms of today’s dollars. To do this, enter the amount in today’s dollars in the amount field to the right and ensure that field is selected, then click the yellow converter icon near the upper left corner of this screen, answer the pop-up questions, and your today’s $ value will be replaced with the equivalent value in future $.

Annual % Increase: The annual rate of increase, and it can be real or nominal. If real, the income stream will increase at the rate of inflation + the real percentage increase; otherwise, the income stream will increase at the specified nominal rate.

Annual % Increase Real or Nominal? Check this box if annual increases are specified in Nominal amounts. If not checked, they’re assumed to be Real and the income stream will increase annually at the rate specified + general inflation.

% of Taxable Rolled Over to Traditional IRA: Taxes on this amount will be deferred until withdrawn from the IRA. For a given pension, this and the option to roll over funds to a Roth IRA are normally mutually exclusive (you can do one or the other).

% of Taxable Rolled Over to Roth IRA: Taxes on this amount will be paid in the year received. For a given pension, this and the option to roll over funds to a traditional IRA are normally mutually exclusive (i.e., you can do one or the other).

Annual Non-taxable Amount: This is the reimbursement of employee contributions to this pension, if any. Contributions are assumed to have been paid with after-tax dollars, so this portion of the pension is not taxed.

Survivor %: Under this pension option, this percentage of all components of this pension will continue after the death of the pension owner for the lifetime of the beneficiary spouse. This and the C&C Period are mutually exclusive (you can specify one or the other, but not both).

Certain & Continuous Period: Under this pension option, all components of this pension will continue for the owner’s lifetime or the specified period, whichever is greater. This and the Survivor % are mutually exclusive (you can specify one or the other, but not both).

Pension Type: This is a pull-down option field that allows you to specify whether this is a private, military or government pension and is relevant only to the calculation of state income tax (state tax codes vary on the deduction of pension income).

Special purpose fields:

These fields are used by Pralana when calculating Oregon and Kentucky taxable income. These states allow a portion of certain pension income to be excluded from state taxable income:

Oregon: Federal pension deduction for pension amounts earned from service prior to 10/1/1991 (subtraction code 307).

Kentucky: Pension exclusion for benefit earned from service before 1998.

State: Select a state from the dropdown.

% State deductible: Enter a percentage of the Federally taxable pension amount that is deductible in the selected state.

Today’s to Future Dollar Converter Tool

The pension amount fields should be entered in terms of future dollars; however, Pralana provides an easy-to-use converter to assist you in converting today’s dollars to future dollars for cases where you only have the requested data in terms of today’s dollars. The converter is in the special section at the bottom of the page. You use it by entering a value in today’s dollars and the future year for which you want it converted to future dollars, then clicking the Calculate button. Pralana will then convert the value you entered in today’s dollars to future dollars using the inflation rate profile associated with the selected scenario.

Income Projection

This tab shows the calculated Pension Income projection over your scenario years.

Windfalls

Inputs

This section enables you to identify taxable and non-taxable windfalls for both you and your spouse. In the fields provided, simply enter the amount (in future year dollars), the associated year and whether the windfall is taxable or non-taxable. If you know the amount in terms of today’s dollars and need to convert it to future dollars, you can use Pralana’s built-in converter feature conveniently located on this page. Unlike income streams that enable starts and stops on specific dates, the windfall income is strictly identified by the year in which it occurs since, by definition, it is always a one-time event.

You can define multiple windfalls in this section and they can be

associated with either you or your spouse based on the radio button at

the top of the page. At any time, all streams associated with the

selected person will be visible. To create a new windfall, just populate

the “new” row. When you do that, another “new” row will appear to enable

you to add the next stream if desired. To delete a windfall just click

the  on the right side of the column.

on the right side of the column.

Today’s $ to Future $ Converter

The windfall amount fields should be entered in terms of future dollars; however, Pralana provides an easy-to-use converter to assist you in converting today’s dollars to future dollars for cases where you only have the requested data in terms of today’s dollars. The converter is in the special section at the bottom of the page. You use it by entering a value in today’s dollars and the future year for which you want it converted to future dollars, then clicking the Calculate button. Pralana will then convert the value you entered in today’s dollars to future dollars using the inflation rate profile associated with the selected scenario.

Income Projection

This tab shows the calculated Windfall Income cash flow projection over your scenario years.

Other Income Sources

This section allows you to define other income streams such as distributions from trusts, alimony and child support. The amounts entered will usually be positive, but you may also enter negative amounts such as for K-1 passive losses. You must select how the income (loss) will be taxed:

Ordinary Income

Use for: Income taxed at ordinary income rates, including K-1 income for which you have active participation.

Reported on: Schedule 1

Long Term Capital Gains

Use for: Income taxed at favorable LTCG/qualified dividend rates and is subject to IRS rules for LTCG annual loss limits and carry over.

Reported on: Schedule D.

Qualified Dividends